If you’re dealing with back pain, neck stiffness, or chronic headaches, you’ve probably asked yourself: how much does chiropractor cost with insurance? Chiropractic care has become an increasingly popular choice for people seeking natural pain relief and improved mobility without relying solely on medication. But understanding the costs—especially with insurance—can feel confusing.

Just as people researching for invisalign cost without insurance, need clear pricing information, those seeking chiropractic care deserve transparent answers about their expected out-of-pocket costs. The answer to how much does chiropractor cost with insurance isn’t one-size-fits-all. It depends on your specific insurance plan, whether your chiropractor is in-network, how many visits you need, and what types of treatments are performed.

This guide breaks down seven essential facts about how much does chiropractor cost with insurance, including average visit costs, typical copays, coverage limits, and practical ways to save money on your care.

What Is Chiropractic Care?

Before diving into how much does chiropractor cost with insurance, it helps to understand what chiropractic care involves. Chiropractors focus on aligning the spine to improve pain and function, but the benefits extend well beyond treating neck pain and back pain.

Chiropractors are trained to diagnose and treat problems with your musculoskeletal and nervous systems. They can create treatment plans that may include:

- Spinal alignment: Manual spinal adjustments, spinal decompression, or spinal mobilization to reduce strain on the neck and back

- Tissue and muscle therapy: Massage therapy, the Graston Technique, or cupping therapy to improve range of motion and circulation

- Specialized therapies: Dry needling, electrical stimulation, or hydrotherapy to penetrate muscles and stimulate nerves

- Alternative therapies: Acupuncture, reflexology, or craniosacral therapy for holistic pain relief

Summary: Chiropractic Care Basics

• Focuses on spine alignment and nervous system function

• Includes spinal adjustments, muscle therapy, and specialized treatments

• Offers drug-free pain relief for back pain, neck pain, and headaches

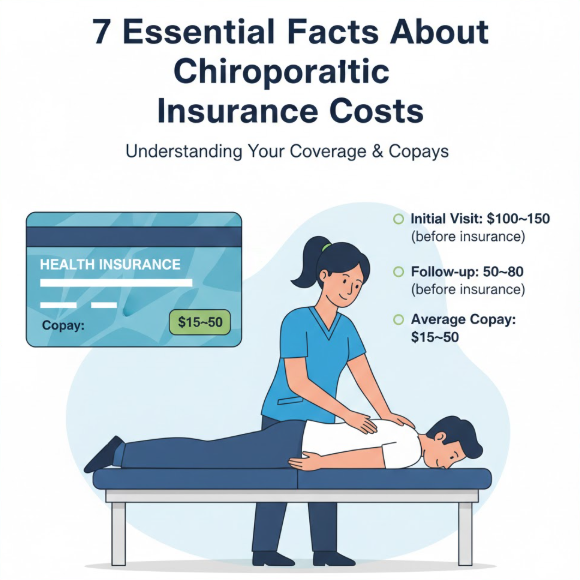

Fact #1: Average Cost of Chiropractic Visits Without Insurance

To understand how much does chiropractor cost with insurance, you first need baseline costs without coverage. This helps you evaluate whether using insurance or paying out-of-pocket makes more sense for your situation.

For those without coverage, understanding cost of removing wisdom teeth without insurance helps put chiropractic costs in perspective—both represent significant out-of-pocket expenses that make insurance valuable.

National Average Ranges:

| Visit Type | Average Cost | Typical Range |

|---|---|---|

| Initial Consultation | $152 | $121 – $281 |

| Follow-Up Visit | $76 | $60 – $140 |

The first visit is more expensive because it typically involves a detailed discussion about your health concerns, medical history, and determining diagnostic or therapeutic procedures.

Cost by State:

Chiropractic costs vary significantly by location. Here are average consultation costs in selected states:

| State | Average Cost | State | Average Cost |

|---|---|---|---|

| California | $189 | New York | $162 |

| Texas | $138 | Florida | $151 |

| Hawaii | $247 | Alaska | $185 |

| District of Columbia | $207 | Illinois | $153 |

Treatment-Specific Costs:

Different chiropractic treatments come with different price tags:

| Treatment Type | Average Cost |

|---|---|

| Manual Spinal Adjustment | $76 |

| Activator Method | $76 |

| Flexion-Distraction Technique | $81 |

| Motorized Decompression (per session) | $101 |

| Deep Tissue Massage | $91 |

| Dry Needling | $51 – $100 |

| Electrical Stimulation | $40 – $126 |

| Acupuncture | $66 – $150 |

Summary: Chiropractic Costs Without Insurance

• Initial visit: $152 average ($121-$281 range)

• Follow-up visit: $76 average ($60-$140 range)

• Costs vary significantly by state and treatment type

• Hawaii highest ($247), Oklahoma lowest ($129)

Fact #2: How Much Does Chiropractor Cost with Insurance? Typical Copays and Coinsurance

Now to the core question: how much does chiropractor cost with insurance? The answer depends on your plan type and whether you visit an in-network provider.

The $15-$50 copays for chiropractic visits are similar to what patients pay when asking how much is laughing gas at the dentist with insurance —both represent routine, predictable out-of-pocket costs for covered services.

Typical Copay Ranges:

| Insurance Plan Type | In-Network Copay | Out-of-Network Cost |

|---|---|---|

| Standard PPO | $20 – $40 per visit | 30-50% coinsurance |

| Medicare Advantage | $15 – $20 per visit | 30% coinsurance |

| Basic Insurance Plans | $30 – $50 per visit | Often not covered |

Real-World Examples:

Blue Cross Blue Shield Federal Plan (Standard Option):

- Preferred provider: $30 copay per visit (no deductible)

- Participating provider: 35% of Plan allowance (deductible applies)

- Non-participating: 35% plus any balance billing

Blue Cross Blue Shield Federal Plan (Basic Option):

- Preferred provider: $35 copay per visit

- Participating/Non-participating: You pay all charges

Johns Hopkins Advantage MD (Medicare Advantage):

- Medicare-covered chiropractic care: $15 copay (in-network)

- Non-Medicare covered chiropractic care: $20 copay (up to 12 visits per year)

Living Well Health Center (Sample Clinic Rates):

- Chiropractic visit with Premera: $60/$6 (deductible/coinsurance)

- Chiropractic visit with Kaiser: $20 copay

- Chiropractic visit with Surest (UHC): $20 copay

Summary: How Much Does Chiropractor Cost with Insurance

• Typical copays range from $15 to $50 per visit

• PPO plans: $20-$40 copays common

• Medicare Advantage: $15-$20 copays typical

• Out-of-network costs significantly higher (30-50% coinsurance)

Fact #3: Insurance Coverage Limits on Chiropractic Visits

When calculating how much does chiropractor cost with insurance, you must consider annual visit limits. Most insurance plans cap the number of covered chiropractic visits per year.

Once you exceed your annual visit limit, you pay 100% out-of-pocket—becomes a significant expense without dental coverage.

Common Visit Limits:

| Insurance Plan Type | Annual Visit Limit |

|---|---|

| Blue Cross Standard Option | 12 visits per year (combined osteopathic/chiropractic) |

| Blue Cross Basic Option | 20 visits per year |

| Johns Hopkins Advantage MD | 12 routine visits per year |

| Typical PPO Plans | 12-20 visits per year |

| Medicare (standard) | Medically necessary spinal manipulation only |

What This Means for Your Costs:

Once you exceed your plan’s visit limit, you pay 100% of costs out-of-pocket—even if you have insurance. This significantly impacts how much does chiropractor cost with insurance for patients needing ongoing care.

Visits That Count Toward Limits:

- Chiropractic spinal manipulation

- Osteopathic manipulative treatment

- Visits you pay for while meeting your deductible

What Medicare Covers:

Medicare covers chiropractic spinal manipulation for an active condition when medically necessary. However, Medicare does NOT cover:

- Examinations

- Decompression/traction

- Manual therapy

- Exercise therapy

- Other adjunct services

Summary: Insurance Coverage Limits

• Most plans cap visits at 12-20 per year

• Once limit reached, you pay full cost

• Medicare covers only spinal manipulation (not exams or therapy)

• Visits paid toward deductible count toward annual limit

Fact #4: Deductibles and How They Affect Your Costs

Your deductible plays a major role in determining how much does chiropractor cost with insurance—especially early in the year.

Just like hot shot trucking insurance, policies have deductibles that must be met before coverage kicks in, health insurance deductibles apply to chiropractic care until you reach your annual limit.

What Is a Deductible?

A deductible is the amount you must pay out-of-pocket before your insurance begins sharing costs. For example, if you have a $500 deductible and chiropractic is covered after deductible, you pay 100% of costs until you’ve paid $500.

Deductible Scenarios:

| Scenario | Your Cost Per Visit | Notes |

|---|---|---|

| Deductible not met | Full cost ($60-$150) | All payments count toward deductible |

| Deductible met, coinsurance applies | 20-50% of negotiated rate | Insurance pays remaining |

| Copay plan (no deductible) | Flat $15-$50 | No deductible to meet |

Plans Without Deductibles:

Some plans, like the Blue Cross Basic Option, have no calendar year deductible for chiropractic care. This means you pay just your copay from the first visit.

High-Deductible Plans:

If you have a high-deductible health plan (HDHP), you may pay full price for chiropractic visits until you meet your deductible—which could be $1,500 or more.

Summary: Deductible Impact

• Before deductible met: You pay full cost

• After deductible met: Insurance shares costs

• Copay-only plans: Best for regular chiropractic users

• HDHPs: May mean paying full price for months

Fact #5: In-Network vs. Out-of-Network Costs

Whether your chiropractor is in-network dramatically affects how much does chiropractor cost with insurance.

Just as patients verify skin md orland park insurances accepted before booking appointments, chiropractic patients should always confirm network participation before their first visit.

In-Network Benefits:

- Negotiated rates (lower than standard fees)

- Copays or coinsurance based on plan

- Provider handles insurance paperwork

- Payments count toward deductible and out-of-pocket maximum

Out-of-Network Costs:

- Higher coinsurance (often 30-50%)

- Deductible typically applies

- May face balance billing (provider charges more than insurance allows)

- You may need to pay upfront and seek reimbursement

Comparison Table:

| Cost Factor | In-Network | Out-of-Network |

|---|---|---|

| Copay/Coinsurance | $15-$40 copay or 10-20% | 30-50% coinsurance |

| Deductible | Often waived for copays | Usually applies |

| Balance Billing | Not allowed | You pay difference |

| Paperwork | Provider handles | You may need to file claims |

Out-of-Network Strategy:

Some chiropractors are intentionally out-of-network because their fees are often less than a typical deductible or copay. They offer “courtesy billing”—submitting claims to your plan so the insurance company reimburses you directly.

Summary: In-Network vs. Out-of-Network

• In-network: Lower costs, less paperwork

• Out-of-network: Higher costs, possible reimbursement

• Some out-of-network providers offer courtesy billing

• Always verify network status before your first visit

Fact #6: When Insurance May Not Cover Chiropractic Care

Understanding exclusions helps you accurately estimate how much does chiropractor cost with insurance for your complete treatment plan.

Unlike elective cosmetic procedures where patients ask does insurance cover breast lift , chiropractic care for active medical conditions is typically covered—but maintenance care falls into a gray area.

Common Non-Covered Services:

| Service | Typical Insurance Status |

|---|---|

| Maintenance/preventive care | Not covered by most plans |

| X-rays for initial exam | Often separate cost |

| Massage therapy | May have separate limits |

| Acupuncture | Often separate benefit |

| Nutritional supplements | Not covered |

| Orthotics | Usually not covered |

Medicare Exclusions:

Medicare specifically does not cover examinations, decompression/traction, manual therapy, exercise therapy, or other adjunct services—only spinal manipulation for active conditions.

Plans That Exclude Chiropractic:

Some insurance plans, particularly basic HMOs or catastrophic plans, may exclude chiropractic coverage entirely. Always verify your specific benefits.

Summary: Non-Covered Services

• Maintenance care often excluded

• X-rays, massage, acupuncture may be separate

• Medicare covers only spinal manipulation

• Some basic plans exclude chiropractic entirely

Fact #7: How to Save Money on Chiropractic Care with Insurance

Even with good insurance, there are strategies to minimize how much does chiropractor cost with insurance.

If you’re shopping for better chiropractic coverage, consider working with insurance brokers to compare plans that offer optimal chiropractic benefits at competitive rates.

Strategy 1: Understand Your Benefits

- Know your visit limits (don’t exceed them)

- Understand your deductible status

- Check if copays count toward out-of-pocket maximum

Strategy 2: Choose In-Network Providers

- Use insurance directories to find covered chiropractors

- Verify network status before booking

- Ask about direct billing capabilities

Strategy 3: Consider Package Deals

Some chiropractors offer package discounts even for insured patients:

- 12-visit package: 10% off

- 24-visit package: 15% off

- Pay per visit vs. package: Compare which saves more after insurance

Strategy 4: Use FSA or HSA Funds

- Flexible Spending Accounts (FSA) and Health Savings Accounts (HSA) cover chiropractic care

- Use pre-tax dollars, saving 20-30% effectively

- Check if your clinic accepts FSA/HSA cards

Strategy 5: Ask About Cash Discounts

For patients with high deductibles, some chiropractors offer cash discounts lower than their standard rates. Compare:

- Insurance copay amount vs.

- Cash pay discounted rate

- Which is lower for your situation?

Strategy 6: Verify Direct Billing

Clinics that offer direct billing to insurance providers mean you don’t have to pay upfront and wait for reimbursement—making chiropractic care more accessible.

Summary: Money-Saving Strategies

• Know your visit limits and deductible status

• Choose in-network providers

• Compare package deals vs. per-visit costs

• Use FSA/HSA for tax savings

• Ask about cash discounts if deductible is high

• Verify direct billing capabilities

Common Misconceptions About How Much Does Chiropractor Cost with Insurance

Misconception 1: “Insurance covers all chiropractic services”

Most insurance covers only spinal manipulation. Exams, X-rays, massage, and therapies may be separate costs or not covered at all.

Misconception 2: “My copay is all I’ll pay”

If you haven’t met your deductible, you may pay full price until you do. Copays typically start only after deductible is met (unless you have a copay-only plan).

Misconception 3: “More visits are always better”

Insurance caps visits at 12-20 per year. After that, you pay 100% out-of-pocket.

Misconception 4: “All chiropractors accept insurance”

Many excellent chiropractors are out-of-network or don’t participate with insurance at all. They may provide superbills for you to file reimbursement.

Misconception 5: “Medicare covers everything”

Medicare covers only spinal manipulation for active conditions—not exams, therapies, or maintenance care.

Summary: Common Misconceptions

• Insurance typically covers only spinal manipulation

• Deductibles affect costs before copays start

• Visit limits mean you pay after 12-20 visits

• Out-of-network providers may still offer reimbursement

Summary: How Much Does Chiropractor Cost with Insurance

Understanding how much does chiropractor cost with insurance requires looking at multiple factors: your plan type, deductible status, network participation, and visit limits.

For more detailed insurance comparisons and provider reviews, visit right insurance lumolog to make informed decisions about your coverage.

Key Takeaways

- Average visit costs: Initial visits average $152; follow-ups average $76 without insurance. With insurance, expect $15-$50 copays after deductible.

- Insurance coverage patterns: Most plans cover chiropractic care but with annual visit limits (typically 12-20 visits per year).

- Deductible impact: If you haven’t met your deductible, you pay full cost until you do. Some plans waive deductibles for copays.

- In-network savings: In-network providers mean lower copays, no balance billing, and less paperwork. Out-of-network costs 30-50% more.

- Coverage limits: Once you exceed your annual visit limit, you pay 100% out-of-pocket—even with insurance.

- Non-covered services: Exams, X-rays, massage, and maintenance care may not be covered. Always verify your specific benefits.

- Money-saving strategies: Use in-network providers, understand your benefits, consider package deals, and use FSA/HSA accounts for tax savings.

The most important takeaway? Never assume—verify. Call your insurance provider, ask about chiropractic benefits (CPT codes 98940-98942 for spinal manipulation), confirm your visit limits, and check network status before your first appointment.

Frequently Asked Questions

1. How much does chiropractor cost with insurance for an initial visit?

With insurance, an initial chiropractic visit typically costs $15 to $50 for the copay, depending on your plan. However, if you haven’t met your deductible, you may pay the full cost ($121-$281) until the deductible is satisfied.

2. Does insurance cover chiropractic maintenance care?

Most insurance plans do NOT cover maintenance or preventive chiropractic care. They typically cover only medically necessary treatment for active conditions. Once your condition stabilizes, further visits may not be covered.

3. How many chiropractic visits does insurance cover per year?

Most plans cover 12 to 20 chiropractic visits per year. Blue Cross Standard Option covers 12 visits, while Basic Option covers 20 visits. Medicare Advantage plans often cover 12-20 visits annually.

4. How much does chiropractor cost with insurance for massage therapy?

If your chiropractor also provides massage therapy, coverage depends on your plan. Some plans include massage under rehabilitation services with similar copays ($20-$60), while others have separate massage benefits or exclude it entirely.

5. Can I use my HSA or FSA for chiropractic copays?

Yes! Chiropractic care is a qualified medical expense for both Health Savings Accounts (HSA) and Flexible Spending Accounts (FSA). You can use these tax-advantaged funds to pay for copays, deductibles, and even full costs if insurance doesn’t cover care.

6. How much does chiropractor cost with insurance if I go out-of-network?

Out-of-network chiropractic care typically costs 30-50% coinsurance after your deductible, plus you may be balance-billed for the difference between the provider’s charge and insurance allowance. This often means paying $60-$150 per visit out-of-pocket.

7. Does Medicare cover chiropractic care?

Medicare covers chiropractic spinal manipulation for active conditions when medically necessary. You pay 20% of the Medicare-approved amount after the Part B deductible. However, Medicare does NOT cover exams, X-rays, massage, or maintenance care.

8. How much does chiropractor cost with insurance for children?

Coverage for pediatric chiropractic care varies by plan. Many plans include children under family benefits with the same copay structure as adults. Verify with your specific insurance provider, as some plans have age restrictions.

References

- Blue Cross and Blue Shield Service Benefit Plan. (2025). Manipulative Treatment Benefits.

- Living Well Health Center. (2026). Pricing – Rehabilitation Services.

- CareCredit. (2025). How Much Does a Chiropractor Cost? Pricing by Treatment.

- Johns Hopkins Advantage MD. (2026). 2026 Plus (PPO) Plan Coverage Details.

- Central Park Chiropractic and Massage. (2025). Fees & Billing – Chiropractic Fees.

- Canyon Springs Chiropractic. (2025). Insurance, Medicare & Billing.

- Peace Chiropractic Arts. (2025). What to Expect: Costs and Insurance.

- Blue Cross and Blue Shield Service Benefit Plan. (2025). Alternative Treatments Benefits.

- RMT Movement. (2025). How Much Does a Chiropractor Cost? Guide to Pricing & Insurance.

Disclaimer: This article is for informational purposes only and does not constitute medical, dental, or insurance advice. Coverage, costs, and benefits vary by provider, plan type, and individual circumstances. Always verify benefits directly with your insurance company using CDT code D9230 and consult your dentist for personalized treatment recommendations. Information is current as of publication date but subject to change.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}