MaxLend loans represent a category of online installment credit products designed for borrowers seeking fast emergency financing. These loans are commonly used when traditional lending channels require longer underwriting cycles. The modern digital lending industry has expanded access to short-term liquidity through automated risk assessment systems.

In the consumer credit ecosystem, maxlend loans occupy a high-risk, high-convenience segment. Borrowers typically choose these products during unexpected medical bills, utility payment delays, or urgent household expenses.

Online direct lenders prioritize speed over long-term repayment optimization. As a result, interest rates are usually higher compared to conventional banking products. The trade-off between accessibility and cost is the defining feature of maxlend loans.

Financial analysts categorize this lending model under alternative consumer finance markets, which primarily serve underbanked populations.

What Are MaxLend Loans

MaxLend loans are unsecured installment loans issued through digital lending platforms. The product is structured to provide rapid cash assistance without requiring collateral assets.

The operational model behind maxlend loans relies on automated underwriting algorithms. Instead of extensive manual verification, lenders evaluate income consistency, banking activity, and repayment probability using data scoring methods.

Many borrowers prefer maxlend loans because credit score thresholds are generally more flexible than traditional financial institutions.

However, consumer finance experts warn that convenience-based lending products often carry elevated annual percentage rates.

The core purpose of maxlend loans is bridging temporary liquidity gaps rather than supporting long-term financial commitments.

Market Position and Industry Context

The short-term installment lending industry has grown significantly due to digital banking adoption. MaxLend loans operate within this expanding fintech-driven consumer credit environment.

Historically, alternative lending emerged to serve individuals who faced rejection from conventional banks. Market data shows that online installment lenders process applications faster because underwriting workflows are automated.

In North America, demand for emergency credit continues rising due to income volatility and unpredictable household expenses.

The competitive landscape of maxlend loans includes payday lenders, microfinance providers, and emerging peer-to-peer credit platforms.

From a regulatory perspective, consumer protection agencies monitor high-interest lending models closely. Transparency in disclosure is considered essential for ethical financial operations.

Key Features of MaxLend Loans

Fast Approval and Funding

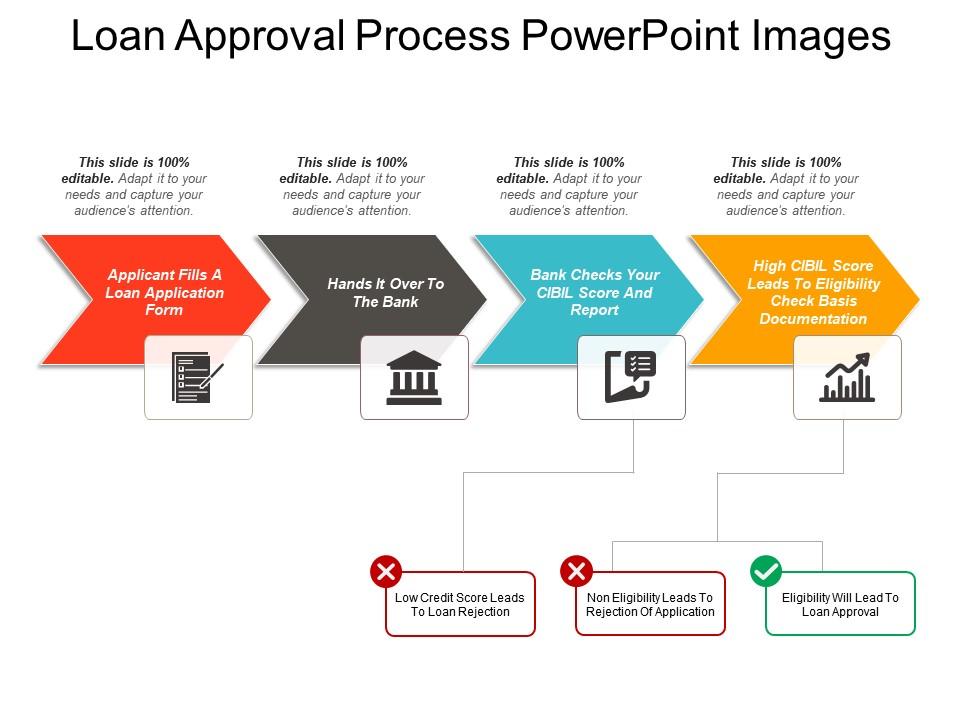

One major advantage of maxlend loans is rapid decision-making. Many applications receive preliminary approval within minutes.

Typical funding timeline:

| Stage | Time Requirement |

|---|---|

| Application submission | 10–20 minutes |

| Automated review | Few minutes |

| Contract approval | Same day |

| Bank deposit transfer | 24 hours (often) |

Speed is achieved through algorithmic credit screening rather than manual financial review.

Credit Score Flexibility

Unlike traditional lenders, maxlend loans may approve borrowers with lower credit scores.

| Credit Profile | Likelihood of Approval |

|---|---|

| Poor credit history | Relatively high |

| Limited credit history | Possible |

| Strong credit profile | Eligible |

Lenders evaluate repayment behavior, income flow, and banking stability.

Unsecured Lending Structure

Maxlend loans usually do not require:

- Property collateral

- Vehicle security

- Investment asset pledges

Unsecured design increases lender risk exposure, which contributes to higher interest pricing.

Interest Rate Structure and Cost Analysis

The cost structure of maxlend loans is one of the most discussed aspects in consumer finance.

Typical APR ranges may vary:

| Loan Profile | APR Range |

|---|---|

| Short term emergency credit | 100% – 300% |

| High risk borrower segment | 300% – 700%+ |

Interest calculation depends on:

- State regulatory rules

- Borrower risk scoring

- Loan term duration

Financial advisors recommend evaluating total repayment obligation before accepting maxlend loans.

Application Requirements

To qualify for maxlend loans, borrowers generally need:

- Age 18 or older

- Active checking account

- Stable income source

- Valid identification

- Residential contact information

Employment verification may be automated or manually reviewed depending on platform policy.

Income stability is a major underwriting signal because installment repayment depends on predictable cash flow.

Risk Factors Associated With MaxLend Loans

Debt Cycle Risk

High-interest short-term lending can create rollover dependency if borrowers fail to manage repayment schedules.

Consumer finance research shows that repeated borrowing increases lifetime interest burden.

Responsible usage of maxlend loans requires emergency-only borrowing behavior.

Payment Default Consequences

Late repayment may lead to:

- Additional penalty fees

- Account collection actions

- Negative credit reporting in some cases

Borrowers should maintain sufficient account balance during automatic debit cycles.

Regulatory and Safety Considerations

The legality of maxlend loans depends on state-level lending authorization.

Consumer protection authorities recommend checking:

- Lender licensing status

- Interest disclosure clarity

- Contract transparency

Digital lending platforms are increasingly required to follow ethical underwriting standards.

Strategic Financial Usage of MaxLend Loans

Financial planners suggest using maxlend loans only for:

- Medical emergencies

- Temporary income interruption

- Essential household expenses

Avoid using high-cost credit products for luxury purchases or speculative investments.

Consumer Experience and Platform Model

The customer experience for maxlend loans is designed around digital convenience.

Common platform features include:

- Mobile-friendly application interface

- Automated decision notification

- Electronic contract signing

- Direct bank integration

Fintech innovation has reduced processing overhead and manual paperwork.

Optimization Points

- Online installment lending provides fast liquidity access

- Approval models rely on automated financial risk scoring

- Interest rates are higher due to unsecured risk structure

- Suitable for urgent short-term financial needs

- Responsible repayment planning is essential when using maxlend loans

Summary

MaxLend loans are online short-term installment loans designed for borrowers needing quick emergency cash. They offer flexible credit requirements and fast funding but typically charge high interest rates. These loans are best suited for temporary financial shortages rather than long-term borrowing.

Takeaway

Fast digital approval system

Flexible credit evaluation

High APR cost structure

Risk of debt dependency if misused

MaxLend Loans – Advantages, Risks, and Financial Impact

Pros and Cons Analysis

| Advantages | Disadvantages |

|---|---|

| Fast funding access | High interest cost |

| Flexible credit screening | Short repayment cycles |

| Simple online application | Potential debt risk |

| No collateral requirement | Penalty fees possible |

The value proposition of maxlend loans lies in accessibility. However, financial responsibility is essential because pricing reflects elevated credit risk.

Comparison – MaxLend Loans vs Other Lending Options

| Feature | MaxLend Loans | Traditional Bank Loans | Credit Card Cash Advance |

|---|---|---|---|

| Approval Speed | Very fast | Slow | Fast |

| Credit Requirement | Low | High | Medium |

| Interest Rate | High | Low–Medium | High |

| Collateral | Not required | Sometimes required | Not required |

| Funding Accessibility | High | Moderate | High |

In modern consumer finance markets, maxlend loans serve borrowers who cannot wait for traditional underwriting cycles.

Repayment Mechanics and Debt Management

Installment repayment is the primary structure used in maxlend loans.

Automatic Payment Model

Most platforms use ACH-based automatic debit systems. This reduces administrative default risk.

Borrowers should follow these best practices:

- Maintain minimum account balance before due date

- Track payment schedules digitally

- Avoid borrowing multiple simultaneous high-cost loans

Financial literacy programs recommend emergency fund reserves equal to at least two repayment installments.

Impact on Credit Behavior

Credit Reporting Effects

Some alternative lenders report repayment behavior to credit bureaus.

Positive repayment history may improve future borrowing credibility.

Late or missed payments can negatively influence credit scoring models.

Credit utilization management is important because revolving debt exposure affects financial risk assessment.

Target Users of MaxLend Loans

Suitable Borrower Profiles

- Individuals facing unexpected expenses

- Workers with irregular income cycles

- People with limited credit history

- Emergency medical expense situations

Not Recommended For

- Long-term debt financing

- Investment speculation

- Lifestyle consumption purchases

Consumer finance advisors emphasize purpose-based borrowing.

Digital Lending Technology Behind MaxLend Loans

Automated Underwriting Systems

Platforms similar to MaxLend use data-driven decision models.

Typical risk scoring inputs include:

- Banking transaction stability

- Income frequency patterns

- Previous repayment behavior

- Identity verification signals

Fintech lending models aim to reduce human bias in credit evaluation.

Regulatory Environment

Online installment lending in the United States operates under state-level oversight.

Financial authorities such as the Consumer Financial Protection Bureau monitor high-interest consumer lending practices.

Key regulatory goals include:

- Transparent APR disclosure

- Fair contract communication

- Anti-predatory lending protection

Borrowers are advised to review state licensing compliance before accepting loan contracts.

Market Role of Alternative Online Lending

The emergence of alternative online lending platforms has transformed modern consumer credit accessibility. Digital short-term lending solutions, including products similar to play a significant role in expanding financial participation among populations that historically faced difficulty obtaining traditional bank financing. These lending models are part of the broader fintech revolution that combines financial services with advanced digital technology.

Financial Inclusion and Credit Accessibility

Digital short-term lending helps bridge financial inclusion gaps by providing credit opportunities to individuals who may not meet conventional banking underwriting standards. Many underbanked or credit-constrained borrowers rely on alternative credit channels because traditional financial institutions typically require strong credit history, stable employment documentation, and higher credit scoring thresholds.

Platforms offering maxlend loans focus on simplifying application procedures while maintaining risk evaluation standards through automated data analysis. This approach allows borrowers with limited financial records to access emergency funding options. In developing and emerging consumer credit markets, alternative lending has become an important mechanism for supporting small-scale economic activity.

Financial inclusion research indicates that access to emergency credit can help households manage unexpected expenses such as healthcare costs, transportation emergencies, or temporary income disruptions. However, experts also emphasize the importance of responsible borrowing education to prevent high-interest debt accumulation.

Role of Underbanked Consumer Financing

A significant portion of alternative lending customers belongs to underbanked demographics. These consumers may lack access to credit cards, personal bank loans, or institutional financing products. Online installment lending providers address this gap by offering digital loan processing systems that reduce administrative barriers.

MaxLend loans and similar products typically utilize streamlined verification methods. Instead of relying heavily on traditional collateral-based lending frameworks, these platforms analyze alternative financial indicators such as transaction stability, income deposit frequency, and account behavior patterns.

The underbanked population often benefits from quick funding cycles. In emergency situations, waiting several business days for conventional loan approval may not be practical. Digital lending ecosystems aim to provide near real-time financial liquidity.

Fintech Innovation and Consumer Behavior Transformation

The growth of fintech lending reflects changing consumer behavior toward mobile and internet-based financial services. Modern borrowers increasingly prefer online application systems that eliminate physical branch visits and reduce paperwork requirements.

Technological integration enables risk modeling improvements in short-term lending operations. Machine learning-based underwriting mechanisms help lenders evaluate repayment probability using historical data trends rather than purely manual financial review.

The popularity of maxlend loans is partly driven by convenience economics. Consumers value speed, simplicity, and accessibility when facing urgent monetary needs. Mobile banking integration, electronic signature verification, and automated deposit processing have significantly improved customer experience.

Economic Impact of Alternative Lending Markets

Alternative online lending contributes to broader financial ecosystem liquidity. Small-scale consumer credit circulation supports retail spending, household stability, and short-term consumption smoothing.

Economists observe that emergency credit availability can reduce financial stress during income volatility cycles. Workers in gig economy sectors, freelance employment structures, and seasonal industries may benefit from flexible borrowing options.

However, policy analysts continue monitoring high-interest short-term lending markets to ensure consumer protection standards. Regulatory agencies such as the Consumer Financial Protection Bureau maintain oversight frameworks to reduce predatory lending practices.

Risk Considerations in Alternative Lending Expansion

While market growth is positive, rapid expansion of online installment lending also introduces financial risk challenges. High annual percentage rates associated with maxlend loans can create repayment pressure if borrowers rely repeatedly on short-term credit.

Debt sustainability remains a major policy concern. Financial education initiatives encourage consumers to evaluate total repayment cost rather than focusing solely on immediate cash availability.

Responsible market development requires balancing credit accessibility with consumer protection mechanisms. Transparent pricing disclosure, ethical underwriting, and borrower awareness programs are essential for long-term industry stability.

Future Trends in Digital Lending

The future of alternative online lending is expected to involve deeper artificial intelligence integration, open banking data sharing, and real-time risk scoring models. Financial technology companies are investing heavily in secure transaction architecture and predictive credit analytics.

Experts predict that digital lending platforms will continue supporting micro-credit ecosystems. Products similar to maxlend loans may evolve toward more personalized repayment structures based on income cycle analysis.

Mobile-first financial services are likely to dominate consumer credit delivery channels. As smartphone penetration increases globally, online installment lending will remain a significant component of retail financial services.

also read: https://fundbulletins.com/hard-money-lender-construction-loan/

Risk Mitigation Strategies for Borrowers

Experts suggest following a structured borrowing approach:

- Calculate total repayment obligation

- Compare multiple lending offers

- Avoid repeat high-interest borrowing

- Maintain emergency savings buffer

Responsible usage improves long-term financial health.

People Also Ask

Are MaxLend loans safe to use?

Yes if borrowed responsibly and repayment terms are understood.

How quickly can I receive funds?

Funding is often completed within 24 hours after approval.

Do MaxLend loans require collateral?

No collateral is typically required.

What is the main risk of MaxLend loans?

High interest cost and short repayment duration.

Can MaxLend loans help improve credit?

On-time repayment may help credit history depending on reporting.

Summary

- Online installment lending supports emergency liquidity needs

- Approval processes rely on automated scoring technology

- Interest rates reflect unsecured lending risk

- Borrowers should evaluate total repayment cost

- Financial planning is essential when using maxlend loans

MaxLend loans are online short-term installment lending products designed to provide rapid emergency cash access for borrowers who may not qualify for traditional banking credit. Offered through platforms such as MaxLend, these loans generally emphasize convenience and accessibility rather than long-term financing. The approval process is usually automated, allowing applicants to receive preliminary decisions quickly compared to conventional financial institutions.

These loans typically require minimal credit history documentation, making them attractive to individuals with poor or limited credit profiles. However, the relaxed underwriting standards are balanced by higher interest rates because the lending model operates as unsecured consumer credit. Since there is no collateral requirement, lenders compensate for potential default risk by pricing loans with elevated annual percentage rates.

Funding speed is one of the primary advantages of maxlend loans, especially for emergency financial situations such as unexpected medical expenses, urgent household repairs, or temporary income interruptions. Many online lending systems use digital transaction verification and risk scoring algorithms to shorten processing time. Borrowers can often complete the application process within minutes using mobile or desktop platforms.

Despite accessibility benefits, financial experts emphasize responsible borrowing behavior when using maxlend loans. Because repayment terms are usually short and interest accumulation can be significant, borrowers should calculate total repayment obligations before accepting loan agreements. Late payment penalties, additional service charges, or account debit failures may increase overall borrowing cost.

Consumer protection organizations including the Consumer Financial Protection Bureau recommend reviewing contract transparency, APR disclosure, and state licensing status before using online installment lenders. Understanding repayment schedules and maintaining sufficient checking account balance during automatic debit cycles can help prevent negative credit reporting or penalty accumulation.

From a financial planning perspective, maxlend loans are best suited for temporary liquidity gaps rather than long-term debt financing. Users should compare multiple lending options, evaluate emergency savings availability, and ensure repayment capacity before committing to high-interest short-term credit products.

Overall, maxlend loans provide fast digital lending access but require disciplined financial management. When used responsibly, they can serve as a practical emergency funding tool, yet borrowers must remain aware of cost structure and repayment obligations.

Conclusion

MaxLend loans provide rapid digital access to short-term financing but come with high interest costs and repayment discipline requirements. They are best used for urgent financial situations rather than long-term borrowing strategies. Understanding cost structure, eligibility factors, and risk exposure helps borrowers make informed decisions.

FAQs

What credit score is needed for MaxLend loans?

No strict minimum credit score is usually required.

Are there hidden fees?

Legitimate lenders must disclose fees in the contract.

Is income verification mandatory?

Generally yes.

Can I repay early?

Early repayment depends on lender policy.

Who regulates MaxLend loans?

State financial regulators and consumer

References

- https://www.consumerfinance.gov

- https://www.ftc.gov/consumer-protection

- https://www.fdic.gov

- https://www.investopedia.com/personal-loans-5180656

- https://www.federalreserve.gov

- https://www.nerdwallet.com

- https://www.usa.gov/credit

Disclaimer:

The content provided is for informational purposes only and does not constitute financial, investment, legal, or tax advice. While efforts are made to ensure accuracy, no guarantees are given regarding completeness or reliability. Any action you take upon the information is strictly at your own risk. We recommend consulting a licensed financial advisor or professional before making financial decisions