When shopping for health coverage, you may come across the term “balanced care insurance” and wonder exactly what it means. The truth is, this phrase can refer to several different types of coverage depending on who you’re talking to. For some, it’s a specific health plan offered through state marketplaces. For others, it’s a completely different type of financial product that combines life insurance with long-term care protection.

Understanding the distinction between these options is crucial because choosing the wrong one could leave you with significant gaps in coverage when you need it most. This guide explores the different meanings of balanced care insurance, what each option offers, and how to make an informed decision for your situation.

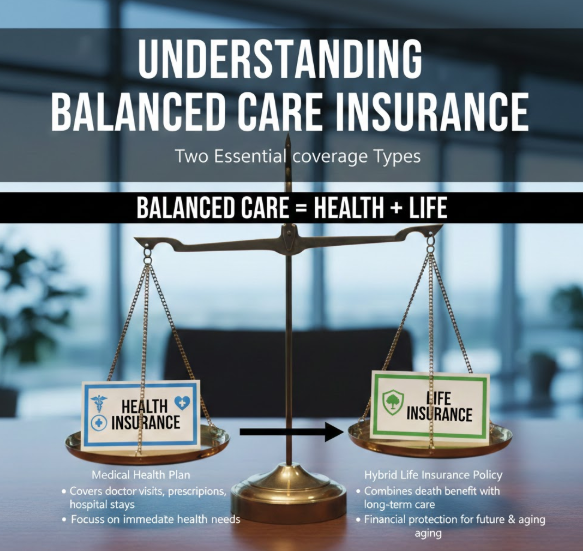

Two Very Different Meanings

The term “balanced care insurance” doesn’t refer to a single product. Instead, it’s used in two distinct contexts:

Ambetter Balanced Care Plans:

These are Affordable Care Act (ACA)-compliant health insurance plans offered through the Health Insurance Marketplace in several states . They provide comprehensive medical coverage with various tiers (like Balanced Care 4, 11, and 32) that differ in costs and benefits . These are legitimate health insurance plans regulated by state insurance departments.

Hybrid Life/Long-Term Care Insurance:

In the financial planning world, “balanced care” sometimes describes hybrid policies that combine life insurance with long-term care benefits . These products let you access a portion of your death benefit to pay for long-term care services if needed, while still leaving something for your beneficiaries if you don’t use the care benefits.

The confusion between these two very different products has led to misunderstandings—and in some cases, unfortunate experiences for consumers who thought they were buying one thing but got another.

Ambetter Balanced Care Plans: What They Offer

For individuals and families seeking comprehensive health coverage through the Marketplace, Ambetter’s Balanced Care plans provide several tiers of coverage. These are legitimate health insurance products regulated under the ACA.

Key Features of Balanced Care Plans:

Balanced Care 4 Example:

One specific plan, Ambetter Balanced Care 4, offers:

- $0 copay for primary care office visits

- $10 specialist copays

- No deductible for many services (deductible applies to hospital and some other services)

- Generic drugs at no charge

- Chiropractic care at $10 per visit (limited to 10 visits yearly)

Balanced Care 32 Example:

At the other end of the spectrum, Balanced Care 32 has higher cost-sharing:

- $45 primary care copay

- $100 specialist copay

- $8,100 individual deductible

- 50% coinsurance after deductible for many services

These plans represent different tiers of coverage, with higher premiums generally meaning lower out-of-pocket costs when you need care.

A Cautionary Note About Non-Insurance Products

While Ambetter’s Balanced Care plans are legitimate health insurance, consumers should be aware that other entities use similar-sounding names for products that are NOT insurance.

Red Flags to Watch For:

Some companies market “health plans” that explicitly state they are not insurance and are not ACA-compliant. These plans may:

- Claim to offer coverage at much lower monthly rates than traditional insurance

- Use confusing terminology to sound like insurance without actually being regulated as such

- Have severe limitations on what they actually pay for

Consumer reviews describe experiences where people purchased what they thought was health insurance, only to discover later that their plan wouldn’t cover needed medications, limited doctor visits to just two per year, and wouldn’t pay for necessary surgery . In some cases, customers were told they couldn’t have surgery until their condition became life-threatening—a situation no legitimate health insurance would create.

One reviewer’s experience captures the frustration: “They do not cover any medications, only pay for 2 doctor visits in a year, and when we planned urgent surgery for my husband… We were told today he cannot have surgery until his inguinal hernia becomes gangrenous” . The fine print in these plans often includes statements like “we are not an insurance company and our plans are not ACA compliant” .

How to Protect Yourself:

Before purchasing any health plan:

- Verify the company is licensed with your state insurance department

- Ask directly: “Is this ACA-compliant major medical insurance?”

- Read the fine print for disclaimers about not being insurance

- Check online reviews from multiple sources

- Be skeptical of prices that seem too good to be true

Hybrid Life Insurance with Long-Term Care Benefits

The other meaning of “balanced care” relates to financial products that combine life insurance with long-term care protection. These hybrid policies offer a different kind of security for those concerned about potential long-term care needs.

How Hybrid Policies Work:

With a hybrid life insurance policy that includes long-term care coverage, you get two potential benefits from one product :

- Long-term care benefits: If you need long-term care, you can access a portion of the policy’s death benefit to help pay for services like home care, assisted living, or nursing facility care

- Life insurance benefits: If you never need long-term care, your beneficiaries receive the full death benefit when you pass away

This structure addresses a common objection to traditional long-term care insurance: the “use-it-or-lose-it” concern where you might pay premiums for years but never use the benefits .

Key Advantages:

What Long-Term Care Covers:

Long-term care includes services people may need if they’re chronically ill or have disabilities—help with activities of daily living like bathing, dressing, eating, and moving around . With costs ranging from around $2,000 monthly for adult day care to nearly $10,000 monthly for nursing home care, having coverage can protect retirement savings .

Who Might Benefit from Each Type

Understanding which type of coverage fits your situation starts with knowing what you need.

Ambetter Balanced Care (Health Insurance) is for:

- Individuals and families needing comprehensive medical coverage

- Those who qualify for ACA subsidies based on income

- People who can work within an HMO network

- Anyone wanting protection against major medical expenses

Hybrid Life/LTC Policies are for:

- People concerned about potential long-term care costs

- Those who want to protect retirement savings from being depleted by care expenses

- Individuals who prefer a product that guarantees some return

- People who can afford the upfront or installment premiums

What to Avoid:

Non-insurance products that claim to offer health coverage but aren’t regulated as insurance. These often appeal to those seeking lower monthly payments but can leave you dangerously exposed when you actually need care.

Questions to Ask Before Buying

Whether you’re considering Marketplace health insurance or a hybrid life/LTC policy, asking the right questions helps ensure you get what you expect.

For Health Insurance:

- Is this plan ACA-compliant major medical insurance?

- What’s the monthly premium, and do I qualify for subsidies?

- What’s the deductible, and what services apply to it?

- Are my doctors and preferred hospitals in-network?

- What are the copays for office visits, prescriptions, and specialist care?

- What’s the maximum I could pay out-of-pocket in a year?

For Hybrid Life/LTC Policies:

- How much long-term care benefit would I have available?

- What triggers qualify me to receive benefits?

- How are benefits paid (reimbursement for expenses or a set monthly amount)?

- What happens to premiums if I never need care?

- Can I get a refund if I change my mind?

- How does this fit with my overall retirement and estate plans?

For Any Coverage:

- Is this company licensed in my state?

- What do independent reviews say about claims-paying history?

- Can I see the complete policy document before purchasing?

Making an Informed Choice

The phrase “balanced care insurance” can lead you down very different paths. One leads to comprehensive health coverage regulated under the ACA. Another leads to financial products designed for long-term care planning. And unfortunately, some paths lead to questionable non-insurance products that may leave you unprotected.

The Bottom Line:

If you’re looking for health insurance to cover doctor visits, hospital stays, and prescriptions, focus on ACA-compliant plans available through your state’s Marketplace. Ambetter’s Balanced Care plans are one legitimate option in this category .

If you’re planning for potential long-term care needs later in life, a hybrid life insurance policy with long-term care benefits might be worth discussing with a trusted financial professional .

What you should avoid are plans that seem too cheap to be true or that include disclaimers about not being insurance. These can cost you far more in the long run—not just in premiums, but in denied care when you need it most .

Conclusion

Navigating the world of health coverage and insurance can feel overwhelming, especially when terms like “balanced care insurance” mean different things in different contexts. The key takeaway is simple: know exactly what you’re buying and who you’re buying it from.

If you need comprehensive medical coverage, Ambetter’s Balanced Care plans offer legitimate, ACA-compliant options worth exploring through your state’s Marketplace. These plans provide the protection you expect from health insurance—coverage for doctor visits, hospital care, prescriptions, and more, with annual limits on your out-of-pocket costs .

If you’re planning for the future and worried about potential long-term care expenses, hybrid life insurance policies with long-term care benefits offer a different kind of protection. They help ensure that if you need care, you have resources to pay for it—and if you don’t, your loved ones still benefit .

What you should never accept is a product that claims to be health insurance but carries disclaimers that it’s not regulated as such. The lower monthly price isn’t worth the risk of discovering—when you’re sick or injured—that your coverage won’t pay for the care you need.

Take time to research, ask questions, and verify licenses. Your health and financial security depend on getting this right.

Frequently Asked Questions

1. Is Balanced Care insurance the same as regular health insurance?

It depends on what you’re referring to. Ambetter’s Balanced Care plans are legitimate ACA-compliant health insurance. However, some non-insurance products use similar names but are not health insurance at all. Always verify the company is licensed and the plan is ACA-compliant.

2. What does Ambetter Balanced Care cover?

Coverage varies by specific plan (e.g., Balanced Care 4, 32). Generally, these HMO plans cover doctor visits, hospital care, prescriptions, preventive services, and more, with costs depending on your plan tier .

3. How much does Balanced Care insurance cost?

Costs vary widely based on the plan, your location, age, and whether you qualify for subsidies. For example, Balanced Care 4 has a $2,650 deductible and $0 copays for primary care, while Balanced Care 32 has an $8,100 deductible and higher copays .

4. What is hybrid long-term care insurance?

This type of policy combines life insurance with long-term care benefits. You can access a portion of the death benefit to pay for long-term care if needed; if you never need care, your beneficiaries receive the full death benefit .

5. How can I tell if a health plan is legitimate?

Check if the company is licensed with your state insurance department. Ask directly if the plan is ACA-compliant major medical insurance. Read all fine print for disclaimers like “not an insurance company” or “not ACA compliant” .

6. Does Medicare cover long-term care?

Medicare generally does not pay for long-term care services like nursing home care beyond very limited, short-term stays. This is why products like hybrid life/LTC policies exist .

7. What should I do if I think I bought a fake insurance plan?

Contact your state insurance department immediately. You can also file a complaint with the Federal Trade Commission (FTC) online or at 877-382-4357 .

References

- eHealth. (2025). Ambetter Balanced Care 4 Plan Summary. https://www.ehealthinsurance.com

- Trustpilot. (2024). mymemberinfo.com Reviews. https://au.trustpilot.com/review/mymemberinfo.com

- KeyHealth Medical Scheme. (2025). Equilibrium Option. https://www.keyhealthmedical.co.za

- HealthMarkets. (2025). Ambetter Balanced Care 32. https://www.dev.healthmarkets.com

- Trustpilot. (2024). mymemberinfo.com Reviews. https://nz.trustpilot.com/review/mymemberinfo.com

- Insurance Informant. (2024). Is Balance Care Health Insurance Legit? https://insuranceinformant.com

- BALANCE Eating Disorder Treatment Center. (2025). Insurance and Financing. https://balancedtx.com

- Brighthouse Financial. (2025). Hybrid Life Insurance and Long-Term Care Policies. https://www.brighthousefinancial.com

- Ambetter Health. (2018). Balanced Care 11 Plan. https://www.ambetterhealth.com

- Cooperative of American Physicians. (2025). Long-Term Care + Life Insurance. https://www.capphysicians.com

Disclaimer:

The content provided is for informational purposes only and does not constitute financial, investment, legal, or tax advice. While efforts are made to ensure accuracy, no guarantees are given regarding completeness or reliability. Any action you take upon the information is strictly at your own risk. We recommend consulting a licensed financial advisor or professional before making financial decisions.