A hard money lender construction loan is a short-term financing instrument used primarily in real estate development and property renovation projects. Unlike conventional mortgages that depend heavily on income verification, this financing model focuses on property value and project feasibility.

Private lending institutions provide this type of credit using collateral-backed underwriting. The property itself serves as primary security, reducing reliance on borrower employment history or traditional credit scoring metrics.

The demand for hard money lender construction loan products has increased among real estate investors who require rapid capital deployment. Developers often prefer this structure when they must secure land acquisition or construction resources quickly.

From a financial architecture perspective, the loan operates within the alternative lending ecosystem, which includes bridge financing and non-qualified mortgage structures.

The approval process for a hard money lender construction loan typically evaluates:

- Property market valuation

- Development blueprint quality

- Exit repayment strategy

- Borrower investment experience

Industry data shows that private construction lending markets expand during periods when traditional banking underwriting becomes restrictive.

Search Intent Behind Hard Money Construction Financing

Most users searching for hard money lender construction loan information fall into three groups:

1. Real Estate Investors

Investors use private lending when they need rapid funding for:

- Fix-and-flip housing projects

- Commercial property upgrades

- Rental portfolio expansion

2. Property Developers

Development companies rely on hard money construction financing when project timelines are aggressive.

3. Borrowers With Non-Traditional Income

Freelancers, small business owners, or international investors may prefer this structure because documentation requirements are lighter.

Market Role of Hard Money Lender Construction Loan Products

4

The financial ecosystem surrounding hard money lender construction loan programs functions as a specialized alternative capital network that operates alongside traditional mortgage banking systems. This private lending environment primarily supports investors, property developers, and construction entrepreneurs who require rapid access to secured financing without undergoing the lengthy underwriting procedures typically associated with institutional banks.

Unlike conventional mortgage structures, which emphasize income verification, employment stability, and long-term credit scoring metrics, private construction lending prioritizes asset collateral strength and project viability. The model allows lenders to evaluate the intrinsic market value of real estate development opportunities rather than relying heavily on borrower financial history.

This alternative capital channel plays a significant role in modern real estate investment cycles. When commercial banking institutions tighten lending requirements due to economic uncertainty, regulatory policy shifts, or monetary interest rate adjustments, private construction financing markets often experience increased activity. Investors seeking development flexibility frequently turn to hard money lender construction loan solutions to maintain project momentum without waiting for conventional loan approval timelines.

The operational framework of private construction financing is built around risk-adjusted capital pricing. Interest rates are typically higher than institutional mortgage products because lenders compensate for reduced documentation requirements, shorter repayment cycles, and elevated project execution uncertainty. However, the higher cost of capital is balanced by the advantage of accelerated funding deployment, which can be critical in competitive property acquisition environments.

Construction developers also benefit from draw-based funding mechanisms commonly associated with hard money lending. Instead of releasing the entire loan amount upfront, capital is distributed in structured stages aligned with verified construction progress. This strategy minimizes financial exposure while ensuring that construction milestones are achieved before additional funding is released.

Another important characteristic of the private lending ecosystem is its adaptability to diverse borrower profiles. Small-scale real estate investors, international property purchasers, and renovation project operators may qualify even when they do not meet strict traditional mortgage eligibility thresholds. This flexibility expands participation in property development markets and supports localized housing construction growth.

From a macroeconomic perspective, private construction lending contributes to housing supply responsiveness. In high-demand urban regions, rapid project financing helps developers initiate construction sooner, which can gradually reduce inventory shortages. Market research from housing finance institutions indicates that alternative lending channels often stabilize development activity during periods of institutional credit contraction.

Overall, the hard money lender construction loan ecosystem represents a complementary financial structure that supports modern real estate development, investment diversification, and construction project liquidity management. Its growing adoption reflects evolving financing preferences in property markets where speed, collateral security, and operational flexibility are prioritized over traditional credit assessment models.

Private construction lending supports housing supply growth in segmented markets where:

- Property demand exceeds institutional lending speed

- Borrowers need flexible underwriting

- Development opportunities require fast capital commitment

Compared to conventional construction credit, hard money construction financing emphasizes collateral quality over borrower income documentation.

Economic research indicates that private lending markets often expand during periods of:

- Interest rate tightening

- Banking regulatory pressure

- High urban property demand

(Based on private capital market behavior studies…)

How Hard Money Lender Construction Loan Approval Works

The underwriting logic behind a hard money lender construction loan differs significantly from government-backed or commercial bank lending.

Step 1. Property Value Assessment

Lenders evaluate:

- Current land or structure value

- Future resale potential

- Local housing market trajectory

Professional appraisal reports are usually required.

Step 2. Project Risk Evaluation

Construction risk factors include:

- Contractor reliability

- Material supply stability

- Timeline feasibility

- Environmental compliance

The primary objective is minimizing default probability.

Step 3. Loan-to-Cost Ratio Calculation

Loan-to-cost (LTC) ratio determines maximum financing exposure.LTC=TotalConstructionCostLoanAmount

Typical construction lending standards:

| Project Type | LTC Limit |

|---|---|

| Residential development | 60% – 80% |

| Small commercial project | 55% – 75% |

| High-risk redevelopment | < 60% |

Private lenders generally avoid overexposure.

Interest Rate Structure of Hard Money Lender Construction Loan

The cost of a hard money lender construction loan reflects risk-based pricing rather than credit history.

Typical Pricing Model

| Component | Range |

|---|---|

| Interest Rate | 8% – 18% annually |

| Origination Fee | 1% – 5% of loan |

| Inspection Draw Fee | Fixed or percentage-based |

| Extension Penalty | Variable |

Interest is often calculated using simple interest rather than compound interest.

Financial analysts note that higher rates compensate for:

- Short repayment duration

- Limited borrower financial disclosure

- Construction execution uncertainty

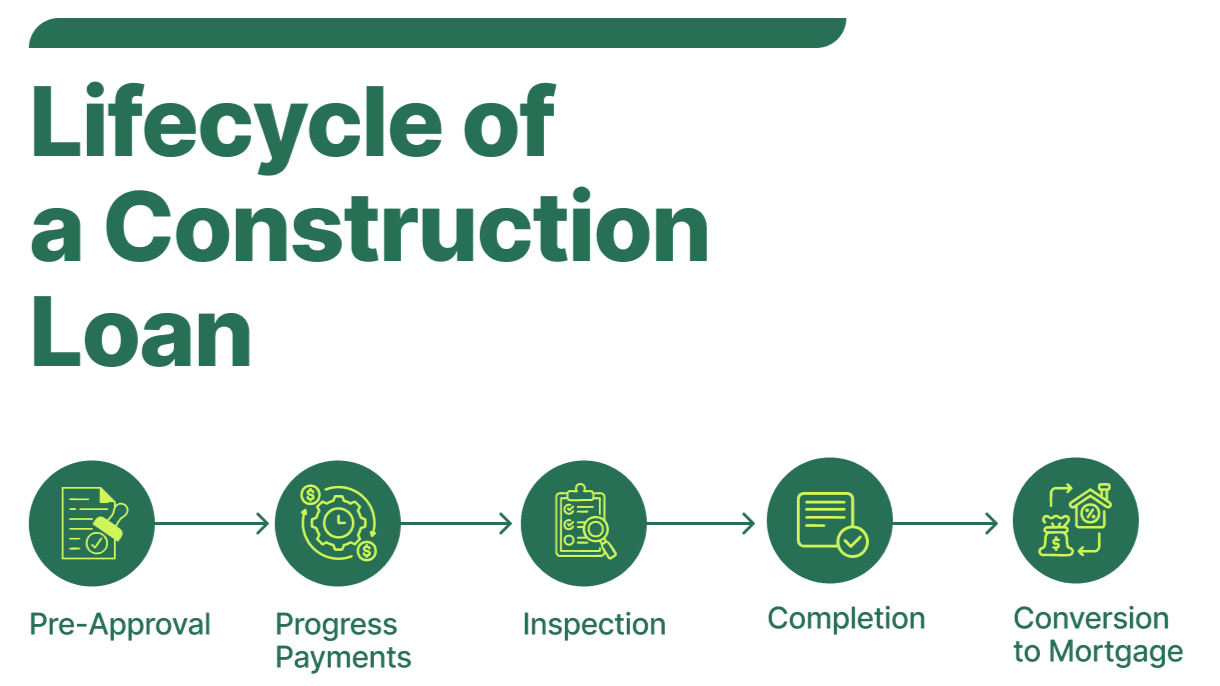

Construction Draw Schedule Mechanics

4

A key feature of hard money lender construction loan programs is staged funding release.

Draw Release Stages

- Foundation completion

- Structural framing

- Roofing installation

- Interior development

- Final inspection approval

Before releasing each draw, lenders may require:

- Site inspection verification

- Contractor progress documentation

- Material usage confirmation

This mechanism protects capital from unfinished project risk.

Qualification Standards for Hard Money Lender Construction Loan

Although credit score is not the dominant factor, lenders still evaluate financial behavior.

Borrower Profile Indicators

| Metric | Importance |

|---|---|

| Property collateral strength | Very High |

| Development experience | High |

| Exit repayment plan | High |

| Credit history | Medium |

| Income documentation | Low |

Many private lenders accept borrowers with moderate credit scores if project security is strong.

Exit Strategy Importance in Hard Money Construction Lending

Exit planning is critical when applying for a hard money lender construction loan.

Common exit mechanisms include:

- Selling completed property

- Refinancing into conventional mortgage products

- Leasing commercial construction projects

A strong exit strategy reduces lender default exposure.

Financial institutions evaluate:

- Local real estate demand

- Price appreciation potential

- Market liquidity conditions

Risks Associated With Hard Money Lender Construction Loan

Interest Cost Pressure

The primary disadvantage of a hard money lender construction loan is higher borrowing cost.

Borrowers should calculate total financing expense before project initiation.

Project Delay Exposure

Construction timeline failure can trigger:

- Extension penalties

- Additional interest charges

- Contract renegotiation

Professional project management reduces execution risk.

Professional Usage Scenarios

A hard money lender construction loan is commonly used in:

- Urban housing redevelopment

- Commercial retail construction

- Residential flipping investment

- Mixed-use property projects

- Land development preparation

Industry practice shows investors prefer private lending when project turnaround time is under 18 months.

Key Takeaway

Asset-based lending dominates approval logic

Fast funding is major competitive advantage

Higher interest compensates for risk exposure

Draw-based construction funding protects lenders

Exit strategy planning improves success probability

also read: https://fundbulletins.com/farm-loan-calculator/

Hard Money Lender Construction Loan – Advanced Market and Strategy Analysis

A hard money lender construction loan is fundamentally different from institutional construction financing provided by commercial banks.

Traditional banking construction loans follow strict regulatory underwriting frameworks that are designed to minimize default risk through comprehensive borrower financial assessment. These institutional lending systems typically require detailed income verification, employment stability records, tax documentation, and long-term credit history evaluation before approval is granted. Debt-to-income ratio compliance plays a significant role in determining borrowing capacity, ensuring that monthly repayment obligations remain manageable relative to the borrower’s financial earnings.

In addition to personal financial assessment, traditional banking construction loans often require adherence to standardized regulatory policies established by financial oversight authorities. Lending institutions must maintain capital reserve requirements and follow consumer protection guidelines that reduce systemic financial risk. This structured underwriting process provides stability to the mortgage finance ecosystem but may also slow down approval timelines, particularly for borrowers who need immediate construction capital.

In contrast, private lending models, especially within the hard money lender construction loan sector, prioritize collateral security and project feasibility over extensive personal financial documentation. The central underwriting philosophy focuses on the tangible market value of real estate assets rather than detailed income behavior patterns of the borrower. Because the loan is primarily secured by property collateral, lenders can evaluate risk based on development potential and liquidation value rather than employment consistency.

Project feasibility assessment becomes a dominant factor in private construction lending decisions. Lenders analyze architectural plans, contractor reputation, construction material reliability, and expected property resale value after project completion. Developers with proven project execution history often receive more favorable financing conditions because their operational performance reduces uncertainty in construction delivery.

Another major distinction lies in approval speed. Traditional bank construction financing may require several weeks or even months due to regulatory compliance checks, internal committee approvals, and extensive documentation validation. Private lenders operating in the hard money lender construction loan market can often finalize preliminary approval within a few days if property collateral valuation meets required thresholds.

Risk pricing also differs significantly between the two systems. Institutional banks usually offer lower interest rates because their underwriting model spreads risk across large borrower portfolios and follows strict regulatory capital management. Private construction lenders charge higher interest rates to compensate for shorter loan duration, higher flexibility, and increased project uncertainty.

Furthermore, private lending provides greater adaptability for borrowers who may not qualify under conventional banking standards. Individuals involved in real estate investment flipping, land redevelopment, or emerging construction entrepreneurship can access funding opportunities that would otherwise be unavailable through traditional mortgage channels.

Overall, while traditional banking construction loans emphasize financial documentation and regulatory compliance, private lending within the hard money lender construction loan market prioritizes asset-backed security, development potential, and rapid capital accessibility, creating a complementary financing pathway in modern real estate development ecosystems.

Major differences include approval speed and documentation intensity.

| Feature | Hard Money Construction Loan | Bank Construction Loan |

|---|---|---|

| Approval Time | 3 – 14 days | 30 – 90 days |

| Documentation | Minimal | Extensive |

| Credit Score Weight | Secondary | Primary |

| Collateral Focus | Very High | High |

| Interest Rate | Higher | Lower |

| Funding Flexibility | High | Moderate |

According to private capital lending research, alternative construction financing supports real estate liquidity when conventional credit markets tighten.

The private lending model is closely associated with the development financing structure used in real estate investment cycles.

Role of Hard Money Lending in Real Estate Investment Ecosystem

The market for hard money lender construction loan products has expanded due to urban property development demand.

Key economic participants include:

- Independent real estate investors

- Property development companies

- Fix-and-flip project operators

- Commercial construction startups

Entities relevant to alternative finance include:

- Federal Housing Finance Agency

- Urban Institute

Private construction lending supports housing supply expansion when institutional mortgage channels become slower.

Research from the Urban Institute shows that flexible credit ecosystems improve small-scale development participation.

Underwriting Metrics Used by Hard Money Lenders

Property Collateral Valuation

Collateral valuation remains the primary approval determinant.

Lenders evaluate:

- Land development potential

- Neighborhood housing price trends

- Construction replacement cost

- Commercial usability

Professional appraisers usually follow standardized valuation frameworks.

Developer Experience Assessment

Experience of project management teams influences approval probability.

Developers with previous successful projects receive:

- Lower interest margin pricing

- Higher LTC approval thresholds

- Faster draw processing

Industry lending behavior shows that experienced borrowers reduce default risk statistically.

Loan-to-Value vs Loan-to-Cost Optimization Strategy

Smart borrowers optimize both metrics.

Loan-to-Value (LTV)

LTV=PropertyMarketValueLoanAmount

Typical ranges:

- Residential development: 65% – 80%

- Commercial project: 55% – 70%

Loan-to-Cost (LTC)

LTC=TotalDevelopmentCostLoanAmount

Lenders prefer conservative LTC exposure to maintain capital protection.

Construction Project Risk Management in Private Lending

Risk control is critical when using a hard money lender construction loan.

Major risk categories:

Market Price Volatility

Real estate price fluctuation affects exit strategy effectiveness.

During economic uncertainty, developers should maintain contingency buffers.

Contractor Execution Risk

Project completion depends on contractor reliability.

Best practices include:

- Performance contract agreements

- Milestone monitoring

- Insurance coverage

Interest Calculation Methods

Private construction lenders usually use simple interest formulas.

Monthly interest expense estimation:Interest=Principal×Rate÷12

Example:

- Loan amount: $300,000

- Interest rate: 12% annually

Monthly cost = approximately $3,000

Borrowers must account for construction timeline delays.

Regulatory Environment and Compliance

Hard money construction loans are generally classified under private lending regulation.

In the United States, oversight involves state-level lending compliance frameworks.

Relevant policy institutions:

- U.S. Department of Housing and Urban Development

- Mortgage Bankers Association

Although private lenders are less regulated than commercial banks, consumer protection laws still apply.

Market Trend Analysis of Private Construction Financing

The demand for hard money lender construction loan products correlates with:

- Urbanization expansion

- Housing inventory shortages

- Investment property speculation cycles

Financial analysts observe increased private lending participation when:

- Central bank interest rates rise

- Traditional mortgage underwriting tightens

According to housing finance market studies, alternative lending channels provide liquidity during credit contraction phases.

Advantages of Hard Money Construction Loans

Speed of Capital Deployment

Fast funding enables:

- Competitive property acquisition

- Early construction initiation

- Market opportunity capture

Flexible Approval Structure

Borrowers may qualify even with:

- Non-traditional income sources

- Moderate credit history

- International investment status

Disadvantages and Cost Considerations

Higher Borrowing Expense

The main tradeoff is interest cost.

Borrowers should perform project return-on-investment calculation before applying.

Short Repayment Duration

Most contracts require repayment within 6–24 months.

Failure to refinance or sell property can create financial pressure.

Investor Strategy Optimization

Professional developers using hard money lender construction loan financing often follow these strategies:

- Maintain 20% contingency construction budget

- Pre-plan exit refinancing channels

- Choose experienced contractors

- Monitor project schedule strictly

Real estate investment success depends on execution discipline.

Summary

- Private collateral-based construction financing

- Faster approval compared to bank construction loans

- Higher interest compensates lending risk

- Draw-based funding reduces unfinished project exposure

- Commonly used in real estate investment development

References

- https://www.hud.gov/program_offices/housing

- https://www.fhfa.gov/

- https://www.urban.org/policy-centers/housing-finance-policy-center

- https://www.mba.org/

- https://www.investopedia.com/terms/h/hard_money_loan.asp

- https://www.consumerfinance.gov/

- https://www.researchgate.net/publication/Private_Lending_Markets_Analysis

- https://www.sciencedirect.com/topics/economics-econometrics-and-finance/real-estate-financing

Disclaimer:

The content provided is for informational purposes only and does not constitute financial, investment, legal, or tax advice. While efforts are made to ensure accuracy, no guarantees are given regarding completeness or reliability. Any action you take upon the information is strictly at your own risk. We recommend consulting a licensed financial advisor or professional before making financial decisions