Understanding Hard Money Loan Calculator

What Is a Hard Money Loan Calculator

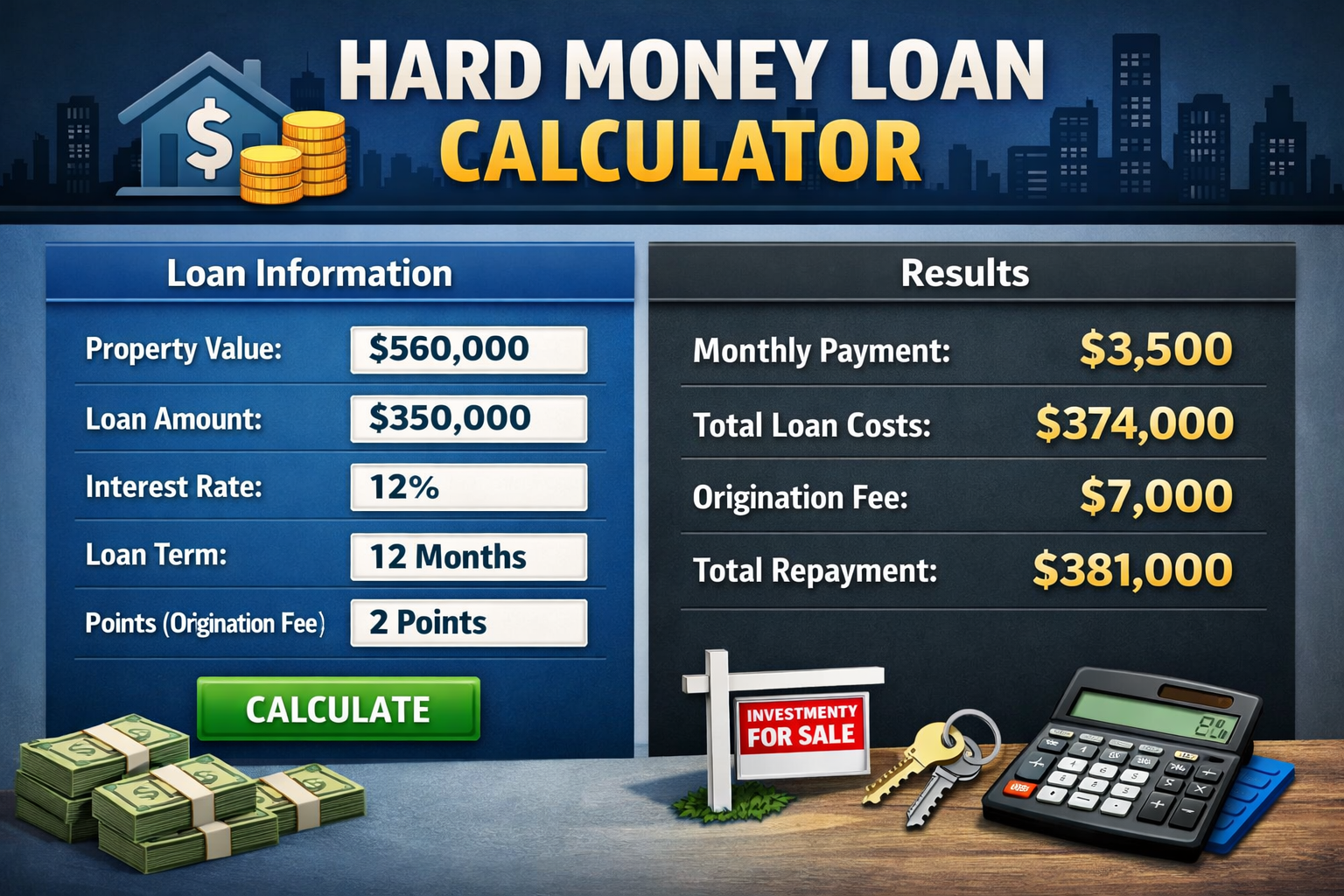

A hard money loan calculator is a financial estimation tool used to predict the cost of short-term, asset-backed private lending. Investors use a hard money loan calculator to evaluate repayment obligations before signing private credit agreements.

The calculator primarily estimates:

- Interest expense over loan duration

- Origination fee impact

- Balloon payment exposure

- Total exit cost risk

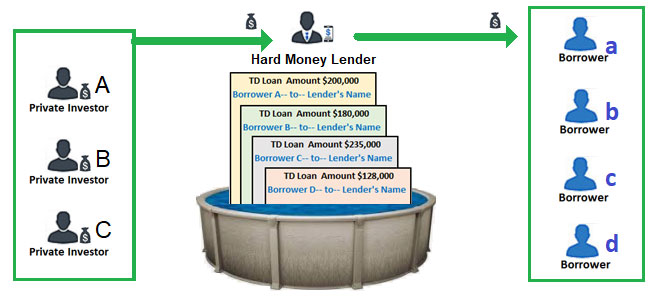

In private lending markets, speed of underwriting matters more than traditional credit scoring. Unlike institutional mortgage models supervised by Federal Reserve System policy frameworks, hard money lending relies heavily on collateral valuation.

A hard money loan calculator is especially useful in real estate investment, property flipping, and bridge financing scenarios. Borrowers use a hard money loan calculator to measure whether expected project profit exceeds financing cost.

Private lenders typically evaluate property security rather than borrower credit profile. This asset-centric model differentiates hard money financing from government-backed mortgage structures supported by agencies such as Fannie Mae and Freddie Mac.

Search-Intent Perspective

Users searching for hard money loan calculator usually want:

- Quick cost estimation

- Investment feasibility analysis

- Short-term financing planning

- Property transaction decision support

Commercial investors and fix-and-flip developers represent the primary audience.

How Hard Money Loan Calculator Works

A hard money loan calculator follows a simplified interest projection model rather than full amortization.

The calculation structure is:

Total Cost = Principal + Interest Expense + Origination Points + Service Fees

Interest Calculation Method

Most private lenders apply simple interest, meaning interest is charged only on principal.

Formula:

Interest Cost = Principal × Rate × Time

Where:

- Rate is annual or monthly interest rate

- Time is loan duration expressed in years

Because many hard money contracts are short term, compounding effects are minimal compared to long-term mortgage products.

A hard money loan calculator helps investors forecast cash flow pressure during holding periods.

Typical loan duration ranges from 6 months to 24 months.

Market research shows that short maturity private credit reduces systemic exposure risk but increases per-period financing cost.

Hard Money Loan Calculator Input Variables

Principal Amount

Principal is the base borrowed capital.

Example ranges:

| Investment Type | Typical Loan Size |

|---|---|

| Residential Fix-and-Flip | $50,000 – $300,000 |

| Commercial Bridge Finance | $200,000 – $2,000,000 |

| Distressed Property Purchase | Variable |

A hard money loan calculator uses principal as the foundation for interest projection.

Interest Rate Structure

Interest rate is the most influential factor in a hard money loan calculator.

Private lending rates are usually higher because risk exposure is greater.

| Market Condition | Typical Rate |

|---|---|

| Low Risk Collateral | 8% – 10% |

| Medium Risk Property | 10% – 13% |

| High Risk Investment | 13% – 18% |

Interest rate policy is influenced by capital cost trends and macroeconomic liquidity conditions monitored by institutions such as the Federal Reserve System.

Investors should always test multiple rate scenarios inside a hard money loan calculator before committing.

Origination Points Explained

Origination points are upfront lender fees.

One point equals 1% of loan principal.

Example:

- 3 points on $200,000 loan = $6,000 fee.

Hard money loan calculator models include point cost because upfront payment affects project cash flow.

Private credit funds often use point fees to offset rapid underwriting expense.

Loan-to-Value Ratio and Collateral Risk

Loan-to-value ratio (LTV) is critical in private lending.

LTV formula:

LTV = Loan Amount ÷ Property Market Value

Example:

- Property value = $300,000

- Loan amount = $210,000

- LTV = 70%

Higher LTV increases lender risk exposure.

Most private real estate lenders restrict LTV because recovery cost increases if default occurs.

Recovery cost includes:

- Legal enforcement

- Asset storage

- Auction marketing

- Property resale discount

A hard money loan calculator may include risk premium adjustment when LTV exceeds 70%.

Hard Money Loan Calculator and Simple Interest Advantage

Simple interest structure is common in short-term private lending.

Advantages:

- Easy repayment forecasting

- Faster investment decision cycle

- Transparent cost projection

- Reduced compounding complexity

Disadvantages:

- Higher effective annual cost compared to amortized mortgage products.

Traditional housing finance institutions such as Fannie Mae prefer amortization schedules to improve long-term repayment stability. Amortization spreads principal repayment across multiple payment periods, reducing default probability and supporting predictable cash flow management for homeowners. Institutional mortgage programs are generally designed for long-term occupancy financing rather than investment speculation.

In contrast, private short-term lending markets operate using different risk optimization principles. Hard money financing is primarily structured for investment project execution rather than permanent housing ownership. Investors using a hard money loan calculator typically focus on project turnaround speed rather than lifetime borrowing cost minimization.

Amortized mortgage structures calculate payment schedules by dividing principal and interest components across each installment period. This mechanism reduces sudden financial pressure on borrowers and supports macroeconomic housing market stability. Central banking authorities such as Federal Reserve System often monitor mortgage lending patterns because housing credit expansion directly influences monetary transmission channels.

Private lending models are more flexible but carry higher cost structures because underwriting standards are simplified. Hard money lenders assume elevated project risk and therefore require compensation through higher interest margins. The difference between institutional mortgage finance and private bridge financing is mainly determined by time horizon and collateral liquidity.

Investment developers frequently compare financing models before property acquisition. A hard money loan calculator allows scenario testing where investors estimate renovation cost, expected selling price, and holding period expense simultaneously. This helps determine whether short-term borrowing generates positive net present value.

Real estate investment profitability depends on market appreciation, construction quality, and transaction timing. If property market demand declines, holding period may extend, increasing interest accumulation. Therefore, professional investors maintain contingency capital reserves when using private financing instruments.

Economic liquidity conditions also influence private lending pricing. When monetary policy tightens, capital availability decreases and interest rates tend to rise. Conversely, expansionary monetary policy can reduce private credit yield pressure. Monitoring signals from institutions like Federal Reserve System helps investors forecast financing cost trends.

Modern real estate investment strategy integrates digital calculation tools. A hard money loan calculator is often embedded inside property investment platforms to provide instant cost estimation. Developers use these calculations during auction bidding, redevelopment project planning, and distressed property purchase evaluation.

Portfolio investors usually evaluate three primary variables before committing capital: collateral quality, exit liquidity, and expected sale price appreciation. Without proper evaluation, high-interest private financing may erode profit margin even if property resale price increases.

Market analysts emphasize that private bridge financing serves as transitional capital rather than permanent debt solution. Borrowers should plan refinancing pathways or property liquidation strategies before loan maturity.

Overall, understanding institutional mortgage models and private lending mechanics improves financial decision-making when using a hard money loan calculator.

Balloon Payment Mechanism

Many hard money loan contracts include balloon payment requirements.

Balloon payment = Remaining principal due at maturity.

Example structure:

| Payment Type | Description |

|---|---|

| Monthly Payment | Interest-only |

| Final Payment | Principal + remaining charges |

Investors must ensure exit liquidity before maturity.

Without exit planning, refinancing or property sale becomes necessary.

Hard Money Loan Calculator for Real Estate Flipping

Property flipping is one of the largest use cases.

Flipping strategy involves:

- Purchase undervalued property

- Renovate asset

- Sell at higher price

- Repay loan principal and interest

Project profit must exceed:

- Interest expense

- Origination points

- Renovation cost

- Transaction tax

Professional investors frequently test multiple scenarios using a hard money loan calculator before acquisition.

Risk Management Considerations

Market Price Volatility

Real estate value fluctuation affects collateral security.

Liquidity Timing Risk

Delayed property sale increases interest burden.

Default Exposure

Private lenders price loans assuming statistically higher default probability compared to institutional mortgage pools.

Credit risk modelling in private lending is less standardized than central banking frameworks such as those monitored by the Federal Reserve System.

also read: https://fundbulletins.com/fnb-calculator-personal-loan/

Hard Money Loan Calculator Usage Summary

A hard money loan calculator serves as a strategic financial planning instrument for investors engaged in short-term real estate financing. The tool helps estimate total borrowing expense by integrating principal amount, interest rate, loan duration, and additional lender charges. Private lending markets rely heavily on asset valuation rather than borrower income verification, which makes such calculators essential for investment feasibility assessment.

Primary Advantages of Hard Money Loan Calculator

Best for Short-Term Investment Financing

Hard money lending is primarily designed for temporary capital deployment. Property developers, fix-and-flip investors, and bridge financing borrowers commonly use this calculation model. Short-term financing reduces long-term interest exposure but requires careful exit planning. Investment cycles typically range between 6 and 24 months depending on property market liquidity.

Works with Asset-Backed Lending Structures

Private lending institutions prioritize collateral security. Loan approval probability depends largely on property valuation rather than credit history metrics. Real estate collateral provides recovery protection in case of borrower default. Asset-backed financing is widely used in redevelopment projects where rapid capital turnover is required.

Uses Simple Interest Estimation Methodology

Most hard money loan calculator models use simple interest projection rather than compound amortization structures. Simple interest means interest is charged only on principal balance. This calculation method simplifies investment forecasting but may result in higher effective annualized cost compared to traditional amortized mortgage systems.

Financial research suggests that simple interest private lending models are more suitable for high-speed capital circulation projects. Institutions such as Fannie Mae typically prefer amortized repayment scheduling because it reduces systemic default risk in long-term housing finance markets.

Origination Fee Projection and Cost Transparency

Origination points are upfront lender compensation charges usually ranging from 1% to 5% of principal value. A hard money loan calculator includes origination fee modeling because upfront charges directly reduce available investment capital.

For example, if a borrower secures a $300,000 private loan with 3 origination points, initial deduction equals $9,000. Developers must account for this cost during renovation budgeting and construction material procurement.

Private lenders justify origination fees because underwriting processes are faster and documentation requirements are minimal. Administrative processing, legal review, and property risk verification contribute to operational cost structures.

Exit Strategy Planning Requirement

A hard money loan calculator is not only a cost estimation tool but also a strategic risk management instrument. Borrowers must confirm repayment source before accepting private financing agreements.

Common exit strategies include:

- Property resale after renovation

- Refinancing through institutional mortgage programs

- Business revenue allocation

- Partnership investment liquidation

Central banking monetary policy signals from institutions such as Federal Reserve System indirectly influence private credit pricing because market liquidity affects capital cost.

Failure to establish exit strategy increases probability of balloon payment default. Many private lending contracts require full principal repayment at maturity, making liquidity forecasting critical.

Hard Money Loan Calculator and Investment Decision Science

Professional real estate investors treat hard money loan calculator outputs as project risk indicators rather than guaranteed cost predictions. Market volatility, construction delays, and property demand changes may affect final repayment burden.

Investment feasibility testing usually involves running multiple simulation scenarios:

- Optimistic property appreciation model

- Conservative market price model

- Worst-case liquidity delay model

If expected sale price minus financing cost is negative, project rejection is recommended.

Economic Role of Private Lending

Private bridge financing supports real estate development speed. When conventional credit underwriting becomes restrictive, alternative financing channels provide liquidity.

Housing finance stability is traditionally associated with long-term amortization structures promoted by institutions such as Fannie Mae. However, entrepreneurial property markets depend on flexible capital access.

Strategic Investment Guidance

Investors using a hard money loan calculator should maintain:

- Debt exposure control

- Property appreciation monitoring

- Construction timeline management

- Cash reserve buffer equal to at least three interest cycles

High-frequency refinancing behavior may increase total repayment burden.

Summary Insight

A hard money loan calculator est[imation tool] helps investors evaluate private lending cost structure, project profitability, and financial risk exposure. It is widely used in short-term real estate investment environments where collateral value drives credit approval decisions rather than traditional income documentation.

Advanced Pricing Structure of Hard Money Lending

A hard money loan calculator is widely used by property investors who require fast financing evaluation before purchasing investment assets. Unlike traditional mortgage underwriting, private lending institutions focus primarily on collateral strength rather than borrower income stability.

Private credit markets operate on risk-adjusted return expectations. Lending cost is determined by project duration, property quality, and market liquidity conditions. Investors rely on a hard money loan calculator to simulate repayment outcomes under multiple interest scenarios.

Interest expense prediction is essential because short-term loans often generate higher annualized cost than conventional housing finance. According to investment finance research, private bridge loans usually target higher yield margins to compensate for rapid capital deployment.

Interest Economics in Private Lending

The pricing model behind a hard money loan calculator reflects credit risk premium theory. When default probability rises, lenders increase interest rates to protect capital recovery potential.

Typical hard money financing interest ranges between 8% and 18% annually. The rate depends on property type, location, and exit strategy reliability. For example, urban commercial redevelopment projects may receive lower rates compared to rural speculative properties.

A hard money loan calculator helps investors evaluate whether project gross profit margin can absorb financing cost. Professional developers often run multiple simulation tests before acquisition.

Market participants compare private lending cost against institutional mortgage benchmarks set historically by organizations such as Fannie Mae and regulatory monetary policy signals from Federal Reserve System.

Origination Fee Impact on Investment Return

Origination points represent upfront processing compensation for lenders. One point equals one percent of principal value.

For example, if loan principal equals $250,000 and origination charge is 3 points, upfront cost becomes $7,500.

A hard money loan calculator should include origination fees because they directly reduce net investment capital available for renovation or purchase.

Private lenders justify point fees due to:

- Fast underwriting approval

- Minimal documentation verification

- Asset-based risk exposure

- Administrative processing expense

Compared to institutional lending programs supported by agencies like Freddie Mac, private financing prioritizes speed over long-term amortization efficiency.

Loan Duration Optimization Strategy

Loan term selection significantly affects repayment burden.

Most private real estate financing operates between 6 and 24 months. Shorter duration reduces total interest cost but increases monthly payment pressure.

A hard money loan calculator assists investors in balancing holding period against renovation completion timeline.

Project developers frequently align loan maturity with expected property sale schedule. If market liquidity slows, refinancing becomes necessary.

Investment analysts recommend maintaining buffer liquidity equal to at least three months of interest expense.

Balloon Payment Risk Management

Balloon payment structure is common in private lending agreements.

Under this structure, borrowers pay:

- Monthly interest installments

- Final principal settlement at maturity

Balloon repayment models are efficient for property flipping businesses.

However, failure to liquidate assets before maturity may cause contract enforcement action.

Default recovery procedures vary by jurisdiction but generally allow lenders to pursue collateral liquidation. Recovery cost includes legal processing, storage, and auction marketing expense.

A hard money loan calculator can project potential loss exposure under worst-case exit scenarios.

Collateral Valuation and Recovery Probability

Collateral value is the primary security mechanism.

Loan approval probability increases when:

- Property location is economically active

- Real estate demand is stable

- Asset condition is structurally sound

Loan-to-value ratio remains a key underwriting parameter.

| LTV Range | Risk Level |

|---|---|

| Below 60% | Low risk |

| 60% – 70% | Moderate risk |

| Above 75% | High risk |

If default occurs, lenders may initiate legal enforcement depending on contract law.

Real estate recovery operations can include resale auctions and negotiated asset transfer.

Investment Decision Modeling

Professional investors treat hard money financing as project capital rather than long-term debt.

A hard money loan calculator helps evaluate:

- Net profit after financing cost

- Renovation expense return ratio

- Sale price forecast margin

- Holding period opportunity cost

Project success depends on accurate property price prediction.

Economic signals from central banking institutions such as Federal Reserve System indirectly influence private lending rates by changing market liquidity.

Responsible Borrowing Framework

Borrowers should follow structured financial discipline when using private financing.

Risk Control Checklist

- Maintain debt-to-income ratio below 40%

- Avoid unnecessary term extension

- Verify lender licensing and contract legality

- Calculate total repayment cost, not only monthly interest

- Ensure exit strategy before loan acceptance

Over-reliance on high-interest private credit can reduce long-term portfolio efficiency.

A hard money loan calculator is therefore considered a planning instrument rather than a borrowing commitment tool.

Market Use Case Statistics Insight

Private bridge financing demand increased significantly in real estate redevelopment markets after tightening of conventional credit underwriting.

Industry research indicates that rapid approval lending models support entrepreneurial property investment cycles.

Developers and real estate funds frequently test financing feasibility using a hard money loan calculator before bidding on distressed assets.

Semantic SEO Summary

Key Topic Coverage:

- Private lending cost modeling

- Real estate investment financing

- Short-term asset-backed credit

- Risk-adjusted interest pricing

- Exit strategy optimization

Primary Audience:

- Property investors

- Fix-and-flip developers

- Bridge financing borrowers

A hard money loan calculator estimates private real estate financing cost by factoring principal, interest rate, origination points, and loan term. It is mainly used for short-term investment projects where collateral property value determines lending approval and repayment risk.

Conclusion

A hard money loan calculator is essential for real estate investors using private short-term financing. It enables precise cost estimation, risk forecasting, and exit strategy planning. Proper calculation improves investment profitability and reduces default exposure.

FAQs

What is a hard money loan calculator?

It is a tool that estimates private lending cost for short-term collateral-based financing.

Why are hard money loans expensive?

Higher risk, faster processing, and limited borrower screening increase pricing.

How accurate is a hard money loan calculator?

It provides estimation; actual cost depends on lender contract terms.

Who uses hard money loans?

Real estate investors, property flippers, and bridge financing users.

What is typical loan duration?

Usually 6–24 months.

References

https://www.federalreserve.gov

https://www.investopedia.com

https://www.nerdwallet.com

https://www.researchgate.net

https://www.hud.gov

https://www.mba.org

Disclaimer:

The content provided is for informational purposes only and does not constitute financial, investment, legal, or tax advice. While efforts are made to ensure accuracy, no guarantees are given regarding completeness or reliability. Any action you take upon the information is strictly at your own risk. We recommend consulting a licensed financial advisor or professional before making financial decisions