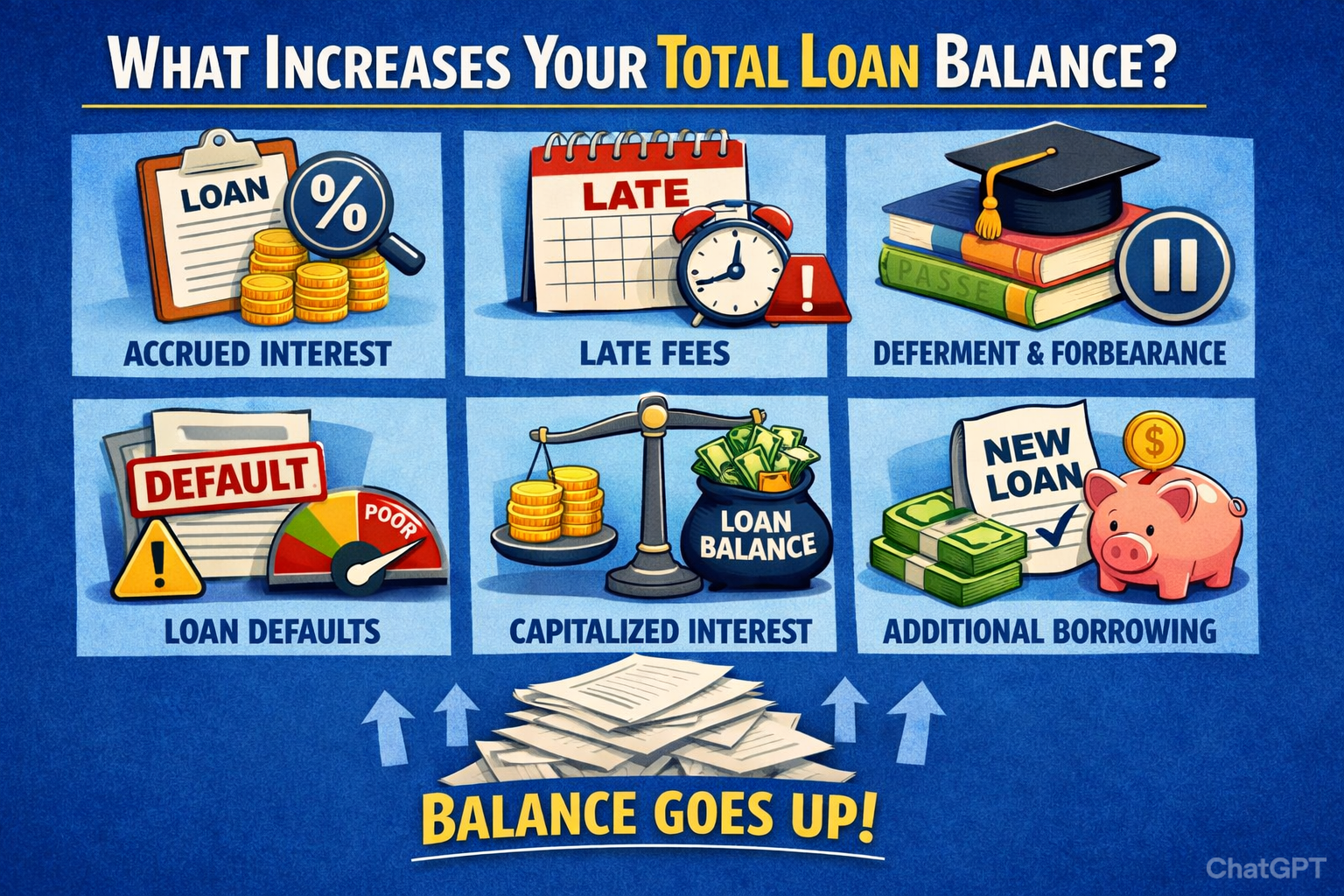

What increases your total loan balance includes accrued interest, compounding, capitalized interest, late payment penalties, administrative fees, and variable rate adjustments. When unpaid interest or fees are added to principal, future interest calculations grow, increasing the overall repayment amount over time.

1. Accrued Interest — The Primary Driver of Loan Growth

Interest accrual is the most fundamental answer to what increases your total loan balance. Every loan agreement includes an interest rate that determines the cost of borrowing. When interest accrues daily or monthly, it adds to the outstanding amount owed until payments are applied.

Lenders calculate interest using:

- Principal balance

- Annual interest rate

- Daily periodic rate

- Compounding frequency

According to the Federal Reserve, interest rates influence the broader cost of borrowing across financial markets. Even small rate differences significantly impact long-term repayment totals.

How Interest Accrues

Most installment loans use this formula:

Interest = Principal × Rate × Time

When payments do not fully cover accrued interest, the remaining portion continues accumulating. This explains what increases your total loan balance even if you are making minimum payments.

Table 1: Simple vs Compound Interest Impact

| Loan Amount | Interest Rate | Term | Simple Interest Total | Compound Interest Total |

|---|---|---|---|---|

| $10,000 | 6% | 5 Years | $3,000 | $3,383 |

| $10,000 | 8% | 5 Years | $4,000 | $4,693 |

| $20,000 | 7% | 10 Years | $14,000 | $16,110 |

Key Insight: Compound interest accelerates what increases your total loan balance because interest is calculated on previously accrued interest.

Internal Summary : How Compounding Works

- Interest accrues daily.

- Unpaid interest remains outstanding.

- Future interest applies to both principal and unpaid interest.

- The longer repayment takes, the larger the growth.

Capitalized Interest — When Interest Becomes Principal

In practical terms, capitalization increases the base amount on which interest is computed. For example, if a borrower has $20,000 in principal and $2,000 in accrued unpaid interest, capitalization increases the principal to $22,000. From that point forward, interest accrues on $22,000 — not the original $20,000. Over time, this compounding effect significantly increases repayment costs.

According to the U.S. Department of Education, capitalization commonly occurs in federal student loans after:

- Grace periods end

- Deferment or forbearance concludes

- Income-driven repayment adjustments occur

- Consolidation of loans

Loan programs administered by Federal Student Aid specify capitalization events within promissory notes and servicing agreements. Once capitalization occurs, the added interest cannot be separated from principal, meaning borrowers pay interest on prior interest for the remainder of the term.

Why Capitalization Increases Long-Term Cost

Capitalization affects repayment in three measurable ways:

- Higher Monthly Payments – Because amortization recalculates using a larger principal.

- Increased Total Interest Paid – Interest compounds on a higher base.

- Extended Repayment Exposure – If payments remain unchanged, payoff time may increase.

Numerical Example of Capitalization Impact

| Original Principal | Accrued Interest | Principal After Capitalization | 10-Year Interest at 6% |

|---|---|---|---|

| $30,000 | $3,600 | $33,600 | $11,184 |

| $30,000 | $6,000 | $36,000 | $11,976 |

Even though no new funds were borrowed, capitalization alone increases total repayment obligations. This mechanism is a central structural explanation of what increases your total loan balance, especially during repayment pauses or reduced-payment plans.

When Capitalization Does Not Occur

Not all loans capitalize interest automatically. Some private lenders may allow unpaid interest to remain separate, and certain subsidized federal loans may cover interest during specific deferment periods (based on program eligibility and policy guidelines).

However, once interest capitalizes, the financial effect is long-term and cumulative. Borrowers often underestimate its impact because capitalization happens at specific trigger points rather than continuously, making it less visible but financially significant.

Key Takeaway

Capitalization does not simply add a temporary charge — it permanently raises the principal. Because future interest is calculated on this higher amount, capitalization is one of the most powerful structural factors behind what increases your total loan balance over time. — When Interest Becomes Principal

This commonly happens during:

- Deferment

- Forbearance

- Grace periods

- Income-driven repayment adjustments

According to U.S. Department of Education, capitalization events can substantially raise repayment totals, particularly in federal student loans administered by Federal Student Aid.

Table 2: Capitalization Cost Example

| Original Principal | Accrued Interest | New Principal After Capitalization | 10-Year Interest at 6% |

|---|---|---|---|

| $25,000 | $3,000 | $28,000 | $9,324 |

| $25,000 | $5,000 | $30,000 | $9,990 |

Capitalization magnifies what increases your total loan balance because interest is recalculated on a higher principal base.

⚠ Capitalization Warning Box

If unpaid interest is capitalized:

- Monthly payments increase.

- Total interest cost increases.

- Repayment timeline may extend.

3. Late Payment Fees and Penalty Charges

Late payments directly contribute to what increases your total loan balance. Most lenders assess fixed or percentage-based late fees when payments exceed a grace period.

According to the Consumer Financial Protection Bureau, late fees can range from $25 to $50 or 4%–6% of the overdue amount depending on the loan type.

Additional Impacts of Late Payments

- Penalty APR increases

- Compounding on unpaid fees

- Collection costs

- Negative credit reporting under the Fair Credit Reporting Act

When fees are added to the outstanding amount, they become part of what increases your total loan balance over time.

Internal Example: One Missed Payment

If a $400 payment is missed on a 7% loan:

- $58 accrues in interest (example basis)

- $35 late fee applied

- Next month interest applies to higher amount

The cumulative effect illustrates what increases your total loan balance even after a single delinquency.

4. Loan Origination and Administrative Fees

Fees are often underestimated when analyzing what increases your total loan balance. Origination fees are typically deducted from disbursed funds but remain part of the total repayment obligation.

Common fees include:

- Origination fee (1%–8%)

- Processing fee

- Underwriting fee

- Servicing charges

- Prepayment penalty (in some loans)

Mortgage and installment loan contracts often incorporate these fees into amortization schedules.

Table 3: Common Loan Fees Comparison

| Loan Type | Origination Fee | Late Fee | Prepayment Penalty | Balance Impact |

|---|---|---|---|---|

| Mortgage | 0.5%–1% | $25–$50 | Sometimes | Moderate |

| Personal Loan | 1%–8% | $15–$40 | Rare | Moderate–High |

| Student Loan (Federal) | ~1% | Varies | None | Low–Moderate |

Even when fees seem small, they compound through interest calculations, contributing to what increases your total loan balance.

Quick Takeaway

Fees may not change your interest rate, but they increase the amount financed. A higher financed amount results in more total interest paid.

5. Variable Interest Rates and Market Adjustments

Variable rates are another structural factor behind what increases your total loan balance. Unlike fixed-rate loans, variable-rate products adjust periodically based on benchmark indices.

Common benchmarks include:

- Secured Overnight Financing Rate

- Federal Reserve target rate

A variable loan typically uses:

Interest Rate = Index + Margin

If the index increases, the borrower’s rate increases accordingly. This leads to higher interest accrual, accelerating what increases your total loan balance.

Table 4: Fixed vs Variable Rate Over 10 Years

| Loan Amount | Initial Rate | Type | Total Interest Paid |

|---|---|---|---|

| $50,000 | 5% Fixed | Fixed | $13,639 |

| $50,000 | 4% → 7% | Variable | $17,880 |

Observation: Even moderate rate adjustments significantly affect repayment totals.

Internal Insight Box

Variable rates introduce uncertainty:

- Payment amounts may rise.

- Long-term cost becomes unpredictable.

- Balance reduction slows during high-rate cycles.

6. Deferment and Forbearance Periods

Deferment and forbearance often explain what increases your total loan balance during temporary hardship periods. While payments pause, interest frequently continues accruing.

In unsubsidized federal student loans:

- Interest accrues daily.

- Unpaid interest may capitalize after deferment ends.

During the COVID-19 emergency relief period under the CARES Act, interest was temporarily set to 0% on eligible federal loans. However, outside such exceptional policies, interest typically accumulates.

Example: 12-Month Forbearance Impact

| Principal | Interest Rate | Interest Accrued in 12 Months | New Balance After Capitalization |

|---|---|---|---|

| $30,000 | 6% | $1,800 | $31,800 |

This demonstrates clearly what increases your total loan balance when payments are paused but interest continues.

Summary

The core financial mechanisms behind loan growth include:

- Accrued interest

- Compounding

- Capitalized interest

- Late fees

- Administrative charges

- Variable rate increases

- Deferment interest accumulation

Each factor either increases principal or raises interest exposure, which directly affects what increases your total loan balance over time.

Structural and Behavioral Factors That Increase Your Total Loan Balance

Section 1 explained core financial mechanics. This section focuses on structural loan design and borrower behavior that further explain what increases your total loan balance over time.

7. Extended Repayment Terms — Lower Payments, Higher Total Cost

Extending the repayment period is one of the most common structural reasons behind what increases your total loan balance in long-term cost terms. While the principal does not immediately grow, total interest paid rises significantly.

Longer terms mean:

- More months of interest accrual

- Slower principal reduction

- Greater exposure to rate fluctuations

According to standard amortization principles used in mortgage lending, total repayment increases as loan duration increases, even if the interest rate remains constant.

Table 5: 10-Year vs 25-Year Term Comparison

| Loan Amount | Interest Rate | Term | Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| $40,000 | 6% | 10 Years | $444 | $13,280 |

| $40,000 | 6% | 25 Years | $258 | $37,400 |

Key Insight: Lower payments may feel manageable, but they significantly expand what increases your total loan balance in total repayment terms.

Internal Takeaway Box

Term Extension Trade-Off

Pros:

- Lower monthly obligation

- Temporary financial relief

Cons:

- Substantially higher lifetime interest

- Slower debt elimination

- Increased cumulative cost

8. Negative Amortization — When Payments Don’t Cover Interest

Negative amortization directly answers what increases your total loan balance even when you are making payments. It occurs when monthly payments are lower than accrued interest, causing unpaid interest to be added to the principal.

This structure was commonly associated with certain Adjustable-Rate Mortgages (ARMs), including option payment loans.

Key mechanism:

- Interest accrues.

- Payment does not fully cover interest.

- Unpaid portion is added to principal.

- Next month interest is calculated on a higher amount.

Example: Negative Amortization Impact

| Principal | Interest Rate | Monthly Interest | Payment Made | Balance After 6 Months |

|---|---|---|---|---|

| $200,000 | 5% | $833 | $600 | $201,398 |

Even though payments were made, the balance increased. This demonstrates structurally what increases your total loan balance under insufficient payment structures.

Payment Allocation Breakdown

Most lenders apply payments in this order:

- Fees

- Accrued interest

- Principal

If the payment only satisfies fees and interest, principal remains unchanged or grows.

9. Missed or Partial Payments

Missed or partial payments are behavioral drivers of what increases your total loan balance. When borrowers fail to meet full payment obligations:

- Interest continues accruing.

- Late fees are assessed.

- Penalty rates may apply.

- Delinquency status may trigger collection costs.

Credit reporting agencies such as Experian, Equifax, and TransUnion record delinquencies, which can indirectly increase borrowing costs in the future through higher interest rates.

Partial payments are applied first to interest. If interest is not fully covered, principal reduction does not occur. Over time, this pattern accelerates what increases your total loan balance.

also read: https://fundbulletins.com/wp-admin/post.php?post=4090&action=edit

10. Refinancing Costs Added to Principal

Refinancing can reduce interest rates, but it may also contribute to what increases your total loan balance if closing costs are rolled into the new loan.

Common refinance costs include:

- Origination fees

- Appraisal fees

- Title charges

- Underwriting costs

If these costs are added to principal rather than paid upfront, the borrower finances the fees and pays interest on them over time.

Refinance Cost Example

| Original Balance | Refinance Costs | New Principal | Rate | 15-Year Interest |

|---|---|---|---|---|

| $150,000 | $5,000 | $155,000 | 5% | $65,458 |

The additional $5,000 accrues interest over 15 years, contributing to what increases your total loan balance cumulatively.

Refinancing Insight

Refinancing lowers rates only if:

- Rate reduction offsets new fees.

- Term is not excessively extended.

- Closing costs are evaluated against long-term savings.

11. Income-Driven Repayment Plans and Balance Growth

Income-driven repayment (IDR) plans cap monthly payments based on income. However, they can contribute to what increases your total loan balance when payments are insufficient to cover accruing interest.

Under programs administered by Federal Student Aid, IDR plans may:

- Cap payments at a percentage of discretionary income

- Allow unpaid interest to accumulate

- Capitalize under certain conditions

Programs like Public Service Loan Forgiveness may forgive balances after qualifying payments, but borrowers outside forgiveness eligibility can see balances grow over decades.

Example: IDR Growth Scenario

| Principal | Rate | Standard Payment | IDR Payment | Balance After 5 Years |

|---|---|---|---|---|

| $60,000 | 6% | $666 | $300 | $68,400 |

When payments do not match accrued interest, balance growth reflects what increases your total loan balance under income-based caps.

12. Default, Collections, and Legal Costs

Default is a severe contributor to what increases your total loan balance. When loans enter default:

- Collection fees are added.

- Legal expenses may apply.

- Interest continues accruing.

- Wage garnishment or asset liens may occur.

Collection agencies may add fees ranging from 16% to 25% of the outstanding balance, depending on contractual terms and jurisdiction.

According to regulatory oversight by the Consumer Financial Protection Bureau, collection costs can significantly inflate total debt obligations.

Default Cost Illustration

| Principal at Default | Collection Fee (20%) | New Balance | Continued Interest |

|---|---|---|---|

| $20,000 | $4,000 | $24,000 | Accrues |

This escalation demonstrates clearly what increases your total loan balance once default status begins.

Table 6: All Drivers of Loan Balance Growth

| Factor | Immediate Effect | Long-Term Impact | Avoidable? | Risk Level |

|---|---|---|---|---|

| Accrued Interest | Gradual increase | High cumulative cost | No | High |

| Capitalization | Principal increases | Compounded growth | Sometimes | High |

| Late Fees | Balance spike | Ongoing accrual | Yes | Medium |

| Extended Term | Lower payment | Higher total interest | Yes | Medium |

| Negative Amortization | Principal grows | Severe escalation | Yes | High |

| Refinancing Costs | Principal increase | Added interest | Yes | Medium |

| Default Fees | Sharp increase | Legal + credit damage | Yes | Very High |

Conclusion

Understanding what increases your total loan balance requires examining both structural loan terms and borrower behavior. Interest accrual, capitalization, extended repayment periods, refinancing fees, negative amortization, and default costs all contribute to long-term debt growth. While some factors are built into loan design, many are manageable through informed repayment strategies and careful financial planning.

FAQs

1. Why is my loan balance increasing even though I make payments?

If your payments do not fully cover accrued interest, unpaid interest may remain outstanding or capitalize. This process explains what increases your total loan balance despite regular payments.

2. Does deferment increase total loan balance?

Yes. During most deferment or forbearance periods, interest continues accruing. If unpaid, it may capitalize, increasing principal and future interest obligations.

3. What is interest capitalization?

Interest capitalization occurs when unpaid interest is added to the principal balance. Future interest calculations then apply to the higher amount, accelerating loan growth.

4. Can refinancing increase my loan balance?

Yes. If closing costs are rolled into the new loan, the principal increases. Interest is then charged on the higher amount.

5. What is negative amortization?

Negative amortization happens when payments are lower than accrued interest, causing unpaid interest to be added to the loan balance.

6. Do longer loan terms increase total repayment?

Yes. Although monthly payments decrease, extended terms result in more total interest paid over time.

7. How can I prevent my loan balance from growing?

- Pay more than minimum when possible

- Avoid deferment unless necessary

- Monitor capitalization events

- Choose shorter repayment terms

- Prevent delinquency

References

- Federal Reserve – Consumer Credit & Interest Rate Data

https://www.federalreserve.gov/releases/g19/ - Consumer Financial Protection Bureau (CFPB) – Loan Servicing & Fees

https://www.consumerfinance.gov/consumer-tools/ - U.S. Department of Education – Federal Student Loan Interest & Capitalization

https://studentaid.gov/understand-aid/types/loans/interest-rates - Federal Student Aid – Income-Driven Repayment Plans

https://studentaid.gov/manage-loans/repayment/plans/income-driven - Secured Overnight Financing Rate (SOFR) – Federal Reserve Bank of New York

https://www.newyorkfed.org/markets/reference-rates/sofr - Experian – Understanding Credit Reporting & Delinquencies

https://www.experian.com/consumer/education/ - CARES Act Overview – U.S. Department of the Treasury

https://home.treasury.gov/policy-issues/coronavirus/about-the-cares-act

Disclaimer:

The content provided is for informational purposes only and does not constitute financial, investment, legal, or tax advice. While efforts are made to ensure accuracy, no guarantees are given regarding completeness or reliability. Any action you take upon the information is strictly at your own risk. We recommend consulting a licensed financial advisor or professional before making financial decisions