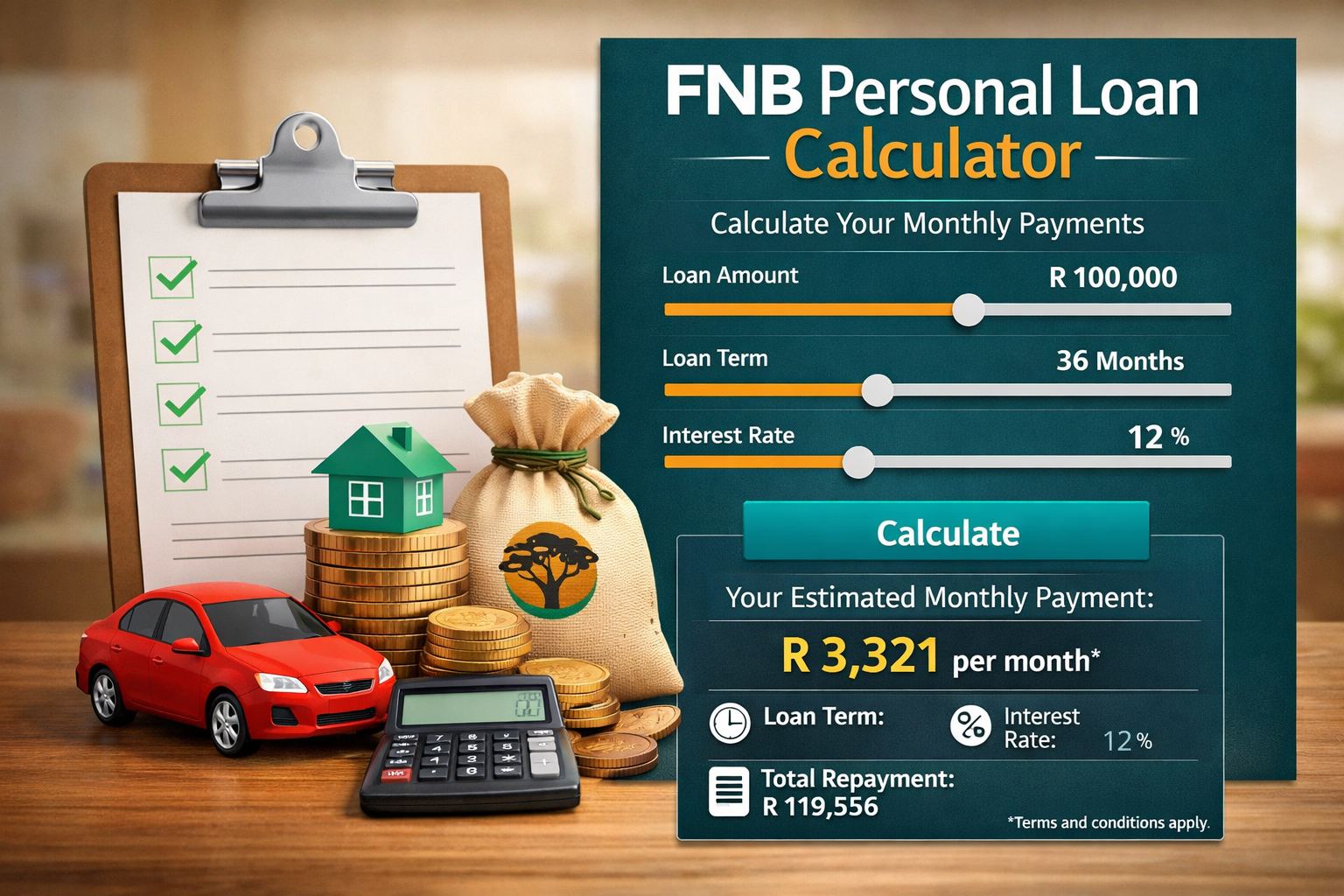

The FNB calculator personal loan tool estimates monthly repayments by inputting the loan amount, repayment term, and interest rate. It uses a standard amortization formula to calculate installment size, total repayment, and total interest cost. Results are estimates and subject to affordability assessment and final credit approval.

What Is the FNB Calculator Personal Loan

The fnb calculator personal loan tool is an online repayment estimation system offered by First National Bank. It allows borrowers to simulate installment amounts before submitting a formal loan application.

It is designed for pre-application financial planning and affordability evaluation. The tool uses standard credit amortization logic to project repayment outcomes based on user inputs.

Purpose of the Calculator

The calculator helps users:

- Estimate monthly installments

- Understand total repayment cost

- Compare repayment terms

- Assess affordability before applying

- Visualize interest impact over time

It is not a loan approval system. It does not guarantee rate qualification or final credit acceptance.

Core Inputs and Outputs

The fnb calculator personal loan system requires three primary inputs:

- Loan amount (principal)

- Loan term (repayment duration)

- Interest rate (APR)

It produces the following outputs:

- Monthly installment

- Total repayment amount

- Total interest payable

Table 1: Inputs vs Outputs Overview

| Category | Variable | Description | Impact |

|---|---|---|---|

| Input | Loan Amount | Principal borrowed | Higher principal increases repayment |

| Input | Loan Term | Duration (months) | Longer term lowers installment but increases total interest |

| Input | Interest Rate | Annual percentage rate | Higher rate increases total cost |

| Output | Monthly Installment | Fixed repayment amount | Determines affordability |

| Output | Total Repayment | Principal + Interest | Reflects full borrowing cost |

How the FNB Personal Loan Calculator Works

The fnb calculator personal loan tool operates using a standard amortization formula commonly applied across consumer lending markets.

The Amortization Formula

Monthly repayment is calculated using:M=P×(1+r)n−1r(1+r)n

Where:

- M = Monthly installment

- P = Loan principal

- r = Monthly interest rate

- n = Total number of payments

This structure ensures:

- Equal monthly payments

- Gradual principal reduction

- Declining interest component over time

(According to industry lending standards used in fixed-rate consumer loans.)

Example Repayment Scenario

Below is a structured estimate using the fnb calculator personal loan methodology.

Table 2: Sample Repayment Estimate

| Loan Amount | Interest Rate | Term | Monthly Payment | Total Repayment |

|---|---|---|---|---|

| R50,000 | 18% APR | 36 months | ±R1,807 | ±R65,052 |

Insight:

Extending the term reduces the installment but increases overall repayment cost due to cumulative interest.

Interest Rates and Pricing Structure

Interest rates for personal loans are influenced by:

- Credit score

- Income stability

- Debt-to-income ratio

- Market prime rate

- Risk-based pricing models

FirstRand Group operates under risk-adjusted lending models aligned with South African credit regulation and prudential banking standards. As the parent company of First National Bank, it applies structured credit risk frameworks that determine pricing, approval thresholds, and capital allocation for unsecured lending products such as those estimated through the fnb calculator personal loan.

Risk-adjusted lending means that interest rates are not fixed uniformly across all borrowers. Instead, pricing is calibrated based on:

- Individual credit score

- Income stability and verification

- Existing debt obligations

- Debt-to-income ratio (DTI)

- Historical repayment behavior

- Macroeconomic risk indicators

These models are developed in accordance with oversight from the National Credit Regulator and broader prudential supervision by the South African Reserve Bank. The objective is to balance consumer access to credit with systemic financial stability and responsible lending obligations under the National Credit Act (NCA).

When a borrower uses the fnb calculator personal loan, the displayed repayment estimate is based on assumed interest inputs. However, during formal underwriting, FirstRand’s internal credit scoring algorithms may adjust the final APR to reflect the applicant’s risk category. Lower-risk profiles typically receive more competitive pricing, while higher-risk profiles may receive higher risk-weighted rates or adjusted loan limits.

From a financial risk management perspective, this approach serves several purposes:

- Capital Protection: Risk-based pricing compensates for potential default probability.

- Regulatory Compliance: Ensures affordability assessments prevent reckless lending.

- Portfolio Stability: Diversifies credit exposure across borrower segments.

- Transparent Cost Disclosure: Aligns with statutory total-cost-of-credit requirements.

In practical terms, the fnb calculator personal loan provides a planning estimate, while FirstRand Group’s risk-adjusted lending framework determines the legally binding loan structure after affordability verification and credit assessment are completed.

Risk-Based Pricing

Under the National Credit Act framework supervised by the National Credit Regulator:

- Higher credit risk results in higher interest rates.

- Lower-risk applicants receive more competitive pricing.

- APR must include all compulsory credit costs.

This ensures transparency in the fnb calculator personal loan output estimates.

Fixed Rate Structure

Most personal loans operate at fixed interest rates:

- Monthly installment remains constant.

- Interest portion declines over time.

- Budget predictability improves.

Variable rates are less common in unsecured personal lending.

Eligibility Requirements for FNB Personal Loans

The fnb calculator personal loan provides estimates, but approval depends on underwriting assessment.

Basic Qualification Criteria

Applicants generally must:

- Be 18 years or older

- Have a valid South African ID

- Show proof of income

- Maintain an active bank account

- Pass affordability checks

Table 3: Qualification Checklist

| Requirement | Purpose |

|---|---|

| Proof of Income | Verify repayment capacity |

| Bank Statements | Confirm cash flow consistency |

| Credit Record | Assess repayment history |

| Identity Verification | Regulatory compliance |

(According to responsible lending practices under South African credit law.)

Factors That Influence Monthly Repayment

Several financial variables directly impact calculator results.

Loan Amount

Higher principal increases monthly obligation.

Loan Term

Longer duration spreads payments but increases interest exposure.

Interest Rate

APR is the primary cost driver.

Existing Debt

High debt-to-income ratio reduces affordability margin.

Credit Profile

Stronger credit lowers risk pricing.

Summary: Repayment Cost Drivers

- Interest rate has the largest long-term impact.

- Term length affects total cost more than installment size.

- Credit profile determines pricing eligibility.

- Shorter terms reduce overall interest burden.

Accuracy of the FNB Loan Calculator

The fnb calculator personal loan provides structured estimates, not guaranteed offers.

Why Final Offers May Differ

Final loan terms may change due to:

- Verified income data

- Updated credit bureau scoring

- Internal risk assessment

- Insurance inclusion

Calculator outputs assume standardized inputs without full underwriting review.

Regulatory Context

The National Credit Act requires:

- Transparent disclosure of total cost of credit

- Full affordability assessment

- Pre-agreement statements

The calculator aligns with these disclosure principles but does not replace formal documentation.

Step-by-Step: How to Use the Calculator

- Enter desired loan amount.

- Select repayment term (e.g., 12–60 months).

- Adjust interest rate if customizable.

- Review monthly installment estimate.

- Compare scenarios by modifying term length.

The fnb calculator personal loan allows scenario testing before commitment.

also read: https://fundbulletins.com/direct-mail-subprime-auto-loan-mailers/

Affordability and Responsible Borrowing

Affordability assessment measures:

- Net monthly income

- Existing debt obligations

- Living expenses

- Credit bureau obligations

Financial institutions must verify that repayment will not cause over-indebtedness.

Responsible Borrowing Checklist

Using the fnb calculator personal loan effectively requires disciplined financial evaluation before submitting a formal credit application. The calculator provides repayment projections, but responsible borrowing decisions must consider long-term affordability, total cost exposure, and regulatory compliance under South African credit standards.

Below is an expanded responsible borrowing framework aligned with consumer credit risk management principles.

Keep Debt-to-Income Ratio Below 35–40%

Debt-to-Income (DTI) Ratio =

Total Monthly Debt Obligations ÷ Gross Monthly Income

Maintaining a DTI below 35–40% reduces financial stress and improves approval probability. A lower DTI indicates stronger repayment capacity and may positively influence risk-based pricing applied after using the fnb calculator personal loan for estimation.

High DTI levels can:

- Trigger affordability concerns

- Reduce eligible loan amount

- Increase interest rate risk premium

- Lead to application rejection

Monitoring DTI before applying ensures realistic borrowing decisions.

Avoid Extending the Term Solely to Lower the Installment

Longer repayment periods reduce monthly installment size but significantly increase total interest paid over time.

For example:

- A 60-month term may appear affordable monthly.

- However, total repayment cost can be materially higher compared to a 36-month structure.

When using the fnb calculator personal loan, always compare:

- Monthly installment

- Total repayment

- Total interest

Term optimization should balance affordability with overall cost efficiency.

Compare Total Repayment, Not Just Monthly Cost

Borrowers often focus only on installment size. This can distort true borrowing cost evaluation.

Key metrics to compare:

- Annual Percentage Rate (APR)

- Total repayment amount

- Total interest payable

- Fees and insurance components

The fnb calculator personal loan allows scenario adjustments to test different terms and amounts. Comparing full repayment totals provides a clearer cost-of-credit perspective.

Consider Early Settlement Flexibility

Personal loans typically use a reducing-balance structure. Making additional principal payments or settling early reduces total interest exposure.

Before applying, confirm:

- Whether early settlement is permitted

- Whether settlement quotes can be requested anytime

- How interest savings are calculated

- If any administrative fees apply

The fnb calculator personal loan shows full-term projections but does not automatically factor in early repayment modeling. Borrowers intending to settle early should evaluate potential interest savings through manual comparison or formal settlement quotations.

Evaluate Income Stability

Affordability assessments review income consistency. Stable employment or predictable cash flow strengthens approval likelihood.

Before applying:

- Ensure payslips reflect stable earnings.

- Avoid applying during income fluctuations.

- Maintain sufficient disposable income buffer after expenses.

Maintain a Healthy Credit Profile

Risk-adjusted pricing frameworks consider:

- On-time payment history

- Credit utilization ratio

- Existing credit exposure

- Length of credit history

Improving credit behavior prior to application may result in better rate offers than those initially estimated through the fnb calculator personal loan.

Summary: Responsible Borrowing Framework

- Maintain DTI below 40%.

- Optimize loan term to reduce total interest.

- Focus on total repayment, not only installment size.

- Use early repayment strategically.

- Confirm full cost disclosure before signing.

Applying these principles ensures that estimates generated by the fnb calculator personal loan translate into financially sustainable borrowing decisions rather than short-term installment relief with long-term cost escalation.

Early Settlement and Additional Payments

Borrowers may reduce total interest by:

- Making additional principal payments

- Settling the loan early

Example: Early Settlement Impact

| Scenario | Remaining Term | Interest Saved |

|---|---|---|

| Settle after 12 months | 24 months avoided | Significant interest reduction |

| Extra R500 monthly | Term shortened | Lower total cost |

(Exact savings depend on outstanding principal balance.)

Key Takeaway

The fnb calculator personal loan tool is a structured pre-application estimation system designed to help prospective borrowers evaluate repayment obligations before entering into a formal credit agreement. It allows users to simulate different borrowing scenarios by adjusting the loan amount, repayment term, and interest rate, producing projected monthly installments and total repayment values based on standard amortization methodology.

By displaying how interest accumulates over time, the calculator enables users to understand the long-term cost implications of extending a loan term or accepting a higher APR. This supports informed financial planning, budgeting accuracy, and debt-to-income ratio evaluation before submitting documentation for credit assessment.

However, the calculator operates purely as an estimation mechanism. It does not perform affordability verification, credit scoring, income validation, or risk-based pricing adjustments that occur during underwriting. Final loan approval, interest rate determination, and maximum loan eligibility are subject to internal risk assessment processes and regulatory compliance requirements under South African credit law.

In summary, the fnb calculator personal loan enhances transparency and cost awareness at the consideration stage but does not replace the formal approval process, affordability assessment, or legally required pre-agreement disclosures.

Early Settlement and Interest Savings Modeling

The fnb calculator personal loan projects repayment obligations across the full selected loan term using a fixed installment amortization structure. It assumes that the borrower will make all scheduled payments until the final maturity date, calculating total repayment and total interest accordingly.

However, personal loans operate on a reducing-balance method. This means interest is calculated only on the outstanding principal at a given point in time, not on the original loan amount throughout the entire term. As monthly payments are made, a portion reduces principal and a portion covers interest. Over time, the principal declines, and the interest portion of each installment becomes smaller.

If a borrower settles the loan early—either through a lump-sum settlement or by making additional principal payments—the remaining balance decreases faster than originally projected. Because future interest is charged only on the remaining unpaid principal, eliminating part or all of that balance reduces the total interest that would have accrued over the remaining term.

For example:

- Paying extra toward principal shortens the repayment period.

- Settling halfway through the term removes all future interest that would have been charged on the remaining installments.

- The earlier the settlement occurs, the greater the potential interest savings.

While the fnb calculator personal loan shows full-term repayment projections, it does not automatically factor in early settlement adjustments. Therefore, borrowers considering prepayment should request a formal settlement quotation to determine the exact outstanding balance and interest savings at a specific date.

In structured financial terms, early settlement converts a long-term amortized obligation into a shortened repayment cycle, reducing cumulative interest exposure and lowering total cost of credit.

How Early Settlement Works

When a borrower settles early:

- Outstanding principal is calculated.

- Accrued interest up to settlement date is added.

- Future interest is removed.

- A settlement quotation is issued.

Interest savings occur because interest is charged only on the remaining principal.

Early Settlement Savings Example

| Remaining Term | Outstanding Principal | Estimated Interest Saved |

|---|---|---|

| 24 months left | R42,000 | ±R8,500 |

| 12 months left | R25,000 | ±R3,200 |

| Extra R1,000 monthly | Term shortened | Lower total repayment |

(Actual values depend on approved rate and timing of payment.)

Key Insight

Early additional payments:

- Reduce principal faster

- Lower total interest

- Shorten repayment duration

The fnb calculator personal loan does not automatically simulate extra-payment scenarios, so manual comparison is recommended.

Regulatory Framework Governing Personal Loans

All South African personal loans operate under the National Credit Act (NCA).

Oversight is provided by the National Credit Regulator, ensuring:

- Transparent disclosure of total cost

- Mandatory affordability assessment

- Clear pre-agreement statements

- Protection against reckless lending

First National Bank operates within this regulatory structure as part of FirstRand Group.

How Long Does Approval Take?

While the fnb calculator personal loan provides instant estimates, approval timelines depend on:

- Document verification

- Income confirmation

- Credit bureau review

- Internal risk scoring

Digital applications may receive preliminary responses within hours. Final disbursement depends on compliance checks.

Documents Required for Application

Although the calculator is estimate-only, formal application requires documentation.

Required Documents:

- South African ID

- Latest payslips (typically 3 months)

- Recent bank statements

- Proof of residence

Self-employed applicants may require additional financial documentation.

How Much Can You Borrow?

Loan limits depend on:

- Verified income

- Credit profile

- Existing obligations

- Internal risk policy

The fnb calculator personal loan allows users to simulate different principal amounts to test affordability before submission.

Does Using the Calculator Affect Your Credit Score?

No.

Using the fnb calculator personal loan does not trigger a credit bureau inquiry because:

- It is a simulation tool

- No formal application is submitted

- No hard credit check occurs

A credit check only happens during a formal loan application process.

Responsible Borrowing Considerations

Personal loans are unsecured credit products. Risk management is essential.

Financial Discipline Guidelines:

- Keep DTI below recommended thresholds.

- Avoid refinancing high-interest debt repeatedly.

- Compare total repayment, not only installment size.

- Confirm early settlement flexibility.

(According to consumer credit risk management practices.)

Frequently Asked Questions (FAQs)

1. How accurate is the FNB personal loan calculator?

The calculator provides amortization-based estimates. Final figures may change after income verification and credit assessment.

2. What interest rate does FNB charge?

Interest rates are risk-based and depend on credit score, affordability, and prevailing market conditions.

3. Can I repay early without penalties?

Early settlement is generally permitted under National Credit Act provisions. Settlement quotes must be requested to confirm final amounts.

4. Does the calculator include fees?

Some estimates may exclude certain initiation or service fees unless specified. Always review the pre-agreement statement.

5. What is the maximum loan term?

Loan terms typically range between short- and medium-term durations depending on internal lending criteria and affordability outcomes.

6. Is the interest rate fixed?

Most personal loans are structured at fixed interest rates for predictable monthly repayments.

Conclusion

The fnb calculator personal loan tool is a structured repayment estimation system that enables financial planning before applying for unsecured credit. It calculates monthly installments, total repayment, and projected interest using standardized amortization methodology. However, final loan terms depend on affordability verification, credit assessment, and regulatory compliance requirements.

Borrowers should focus on total cost of credit, not just installment size, and consider early repayment strategies to reduce overall interest exposure.

References

- First National Bank (FNB) – Personal Loans

https://www.fnb.co.za - National Credit Regulator (South Africa)

https://www.ncr.org.za - South African Reserve Bank – Interest Rate Information

https://www.resbank.co.za - National Credit Act 34 of 2005

https://www.justice.gov.za/legislation/acts/2005-034%20creditact.pdf - FirstRand Group Financial Reports

https://www.firstrand.co.za

Disclaimer:

The content provided is for informational purposes only and does not constitute financial, investment, legal, or tax advice. While efforts are made to ensure accuracy, no guarantees are given regarding completeness or reliability. Any action you take upon the information is strictly at your own risk. We recommend consulting a licensed financial advisor or professional before making financial decisions